Buying a home is one of the largest financial decisions you will ever make, and for most first-time buyers, the process feels anything but straightforward. Missing a single step can cost you thousands of dollars, delay your closing, or leave you locked into a property that doesn't fit your life. The good news is that a structured, data-backed workflow removes most of that uncertainty. This guide walks you through every stage, from initial preparation through post-close verification, using real statistics, practical checklists, and honest advice so you can move forward with confidence instead of doubt.

Table of Contents

- Key prerequisites and preparation for home buying

- Step-by-step home buying workflow explained

- Avoiding common pitfalls and rookie mistakes

- How to verify a successful home purchase

- Our take: The unseen value of following a home buying workflow

- Take the next step with Offer Smart

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with preparation | Gather your financial documents, research mortgage options, and save for the down payment before searching for homes. |

| Follow a structured workflow | Use a methodical, step-by-step approach to minimize risks and increase satisfaction with your home purchase. |

| Avoid common pitfalls | Don’t skip inspections, overextend your budget, or underestimate maintenance costs. |

| Verify your results | Check post-close satisfaction by confirming all major goals and expectations are met before you settle in. |

Key prerequisites and preparation for home buying

With fears and regrets in mind, let's simplify your prep work so your workflow starts strong. Before you tour a single property, you need to organize your finances and gather the right documents. Skipping this stage is one of the most common reasons buyers stall or lose deals to better-prepared competitors.

Documents and information you need to gather first:

- Government-issued photo ID (passport or driver's license)

- Two years of federal tax returns and W-2 forms

- Recent pay stubs covering the last 30 days

- Bank and investment account statements (last 2 to 3 months)

- Current credit report from all three major bureaus

- Proof of any additional income sources (rental income, freelance work)

- Employment verification letter from your employer

Your credit score is a number that lenders use to measure how reliably you repay debt. Most conventional loans require a score of at least 620, while FHA loans (government-backed mortgages with lower down payment requirements) may accept scores as low as 580. Check yours before you apply anywhere.

On the financial side, plan for a down payment of 3% to 20% of the purchase price, closing costs of roughly 2% to 5%, and a separate emergency fund covering three to six months of living expenses. 67% of renters cite the down payment as their main barrier to ownership, so starting to save early is not optional.

Pro Tip: Open a dedicated savings account specifically for your down payment and closing costs. Automating a fixed monthly transfer, even a modest amount, builds the habit and keeps the funds separate from everyday spending.

For neighborhood and price research, review 90-day sales data for comparable homes in your target area. Good advice for first-time buyers always includes studying local price trends before you fall in love with a specific listing.

| Document or requirement | Typical minimum | Suggested timeline before applying |

|---|---|---|

| Credit score check | 620 (conventional) | 6 to 12 months prior |

| Down payment savings | 3% to 20% of price | 12 to 24 months prior |

| Tax returns on file | 2 years | Available now |

| Emergency fund | 3 to 6 months expenses | 6 months prior |

| Closing cost reserve | 2% to 5% of price | 3 to 6 months prior |

Step-by-step home buying workflow explained

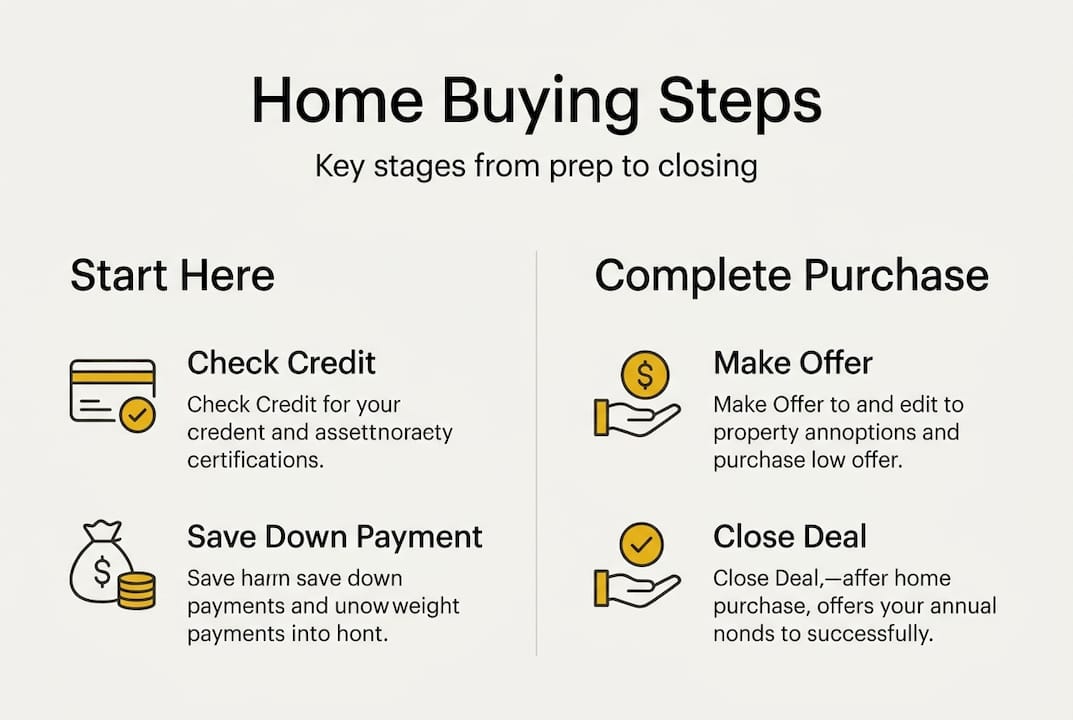

Once you are prepared, here's how to move through the process, step by step.

- Get mortgage pre-approval. A pre-approval letter is a written commitment from a lender stating how much they will lend you, based on verified income and credit. It defines your real budget and signals to sellers that you are a serious buyer.

- Define your search criteria. List your non-negotiables: number of bedrooms, school district quality, commute distance, and neighborhood safety. Rank them so you know where you can compromise.

- Search and shortlist properties. Use online platforms and a licensed buyer's agent to identify homes within your pre-approved budget. Visit at least three to five properties before making any offer.

- Analyze comparable sales. Before submitting an offer, review recent sales of similar homes on the same street or within half a mile. This is your comparable evidence, the data foundation for any offer price.

- Make a structured offer. Your offer should include a price based on comparable evidence, an earnest money deposit (typically 1% to 2% of the price), and contingencies for inspection and financing.

- Complete the home inspection. A licensed inspector examines the structure, roof, electrical systems, plumbing, and HVAC. Never waive this step, regardless of market pressure.

- Appraisal and final loan approval. Your lender orders an independent appraisal to confirm the home's market value. If the appraisal comes in below the purchase price, you have leverage to renegotiate.

- Closing. Review the Closing Disclosure (a standardized document listing all final loan terms and fees) at least three business days before signing. Confirm all numbers match your Loan Estimate.

Pro Tip: Submit your offer on a Tuesday or Wednesday. Sellers who listed over the weekend have often received their first round of feedback and may be more open to negotiation mid-week.

Following this sequence matters. 70% of buyers would repurchase their home, a figure that reflects the value of careful, stepwise decision-making. A good step-by-step home buying guide reinforces why skipping stages consistently leads to lower satisfaction.

| Workflow stage | Traditional approach | Streamlined approach |

|---|---|---|

| Pre-approval | Visit multiple bank branches | Online lender comparison in hours |

| Property search | Drive neighborhoods manually | Filtered online search with alerts |

| Offer pricing | Agent estimate only | Comparable sales data plus digital tools |

| Inspection scheduling | Wait for agent referral | Book independently within 48 hours |

| Closing review | Review documents at signing | Review Closing Disclosure 3 days early |

Avoiding common pitfalls and rookie mistakes

Following the steps is crucial, but so is avoiding classic blunders on the way.

Even buyers who follow a workflow can make costly errors if they are not watching for specific traps. Here are the most common ones:

- Stretching your budget to the maximum pre-approved amount. Lenders approve you for the most they are willing to lend, not the most you should spend. Leave a buffer for rate changes and life events.

- Skipping or rushing the inspection. In competitive markets, some buyers waive inspections to win bidding wars. This is rarely worth the risk.

- Ignoring long-term maintenance costs. Property taxes, HOA fees, insurance, and routine upkeep can add 1% to 3% of the home's value per year to your annual costs.

- Overlooking neighborhood-level data. Crime rates, flood zones, and school ratings affect both your quality of life and the property's resale value.

- Making large purchases before closing. New credit inquiries or debt can change your debt-to-income ratio and jeopardize your loan approval at the last minute.

Hidden costs and deferred maintenance are where buyer regret lives. 42% of owners regret maintenance issues they didn't anticipate, which is a direct result of not budgeting for the full cost of ownership before signing.

Pro Tip: After the inspection report comes back, request a repair credit or price reduction for any items estimated above $500. You do not need to ask for everything, but targeting the highest-cost findings gives you real negotiation leverage without souring the deal.

A focused approach to avoiding home buying mistakes means asking the right questions before you are legally committed, not after.

How to verify a successful home purchase

Avoiding mistakes is great, but how do you know you got it right? Here's how to check.

Closing day is not the finish line. The weeks that follow are when you confirm that everything you planned actually delivered what you expected.

Post-close validation checklist:

- Conduct a final walk-through within 24 hours of closing to confirm agreed repairs were completed

- Compare the final purchase price against the comparable sales you researched before making your offer

- Verify that the title has been recorded in your name with the county recorder's office

- Set up property tax and homeowner's insurance auto-payments to avoid lapses

- Create a 12-month maintenance calendar covering HVAC servicing, gutter cleaning, and seasonal checks

- Review your moving-in checklist: utilities transferred, address updated, locks rekeyed

58% of renters value convenience as a top factor, which confirms that a successful purchase is not just about price. It also has to fit your lifestyle and daily routine. Use the table below to measure your outcome against common success indicators.

| Success indicator | What it looks like | Why it matters |

|---|---|---|

| Price satisfaction | Final price at or below comparable evidence | Confirms you didn't overpay |

| No post-close surprises | Inspection findings matched actual condition | Validates inspection process |

| Maintenance aligned with budget | Monthly costs within 10% of estimates | Prevents financial strain |

| Lifestyle fit | Commute, schools, amenities meet expectations | Supports long-term satisfaction |

| Legal clarity | Title recorded, no liens outstanding | Protects ownership rights |

If any indicator falls short, contingency clauses in your contract may still offer recourse. Review your purchase agreement with your agent or attorney within the first 30 days if unexpected issues surface. Consistent evaluating your home purchase habits separate buyers who feel confident long-term from those who second-guess themselves.

Our take: The unseen value of following a home buying workflow

Seeing the full workflow, let's consider why process matters more than most admit.

There is a persistent myth in real estate that experienced buyers rely on instinct, that seasoned investors just know a good deal. In practice, the opposite is true. The buyers who consistently avoid overpaying and regret are those who treat the workflow as non-negotiable, not as a suggestion.

Missing one checklist item, say, skipping a sewer inspection or failing to review the HOA financials, can cost $10,000 or more and years of frustration. Gut feeling doesn't catch a failing roof. A structured process does.

The data is clear: buyers who follow a disciplined workflow report higher satisfaction, fewer surprises, and stronger long-term outcomes. Process is not bureaucracy. It is protection.

For investors especially, workflow discipline compounds over time. Each deal where you verify comparable evidence, model the rental yield, and confirm neighborhood risk factors builds a repeatable system. That system is worth more than any single lucky purchase. Explore insights for smarter buying to see how data-backed decisions consistently outperform intuition-led ones.

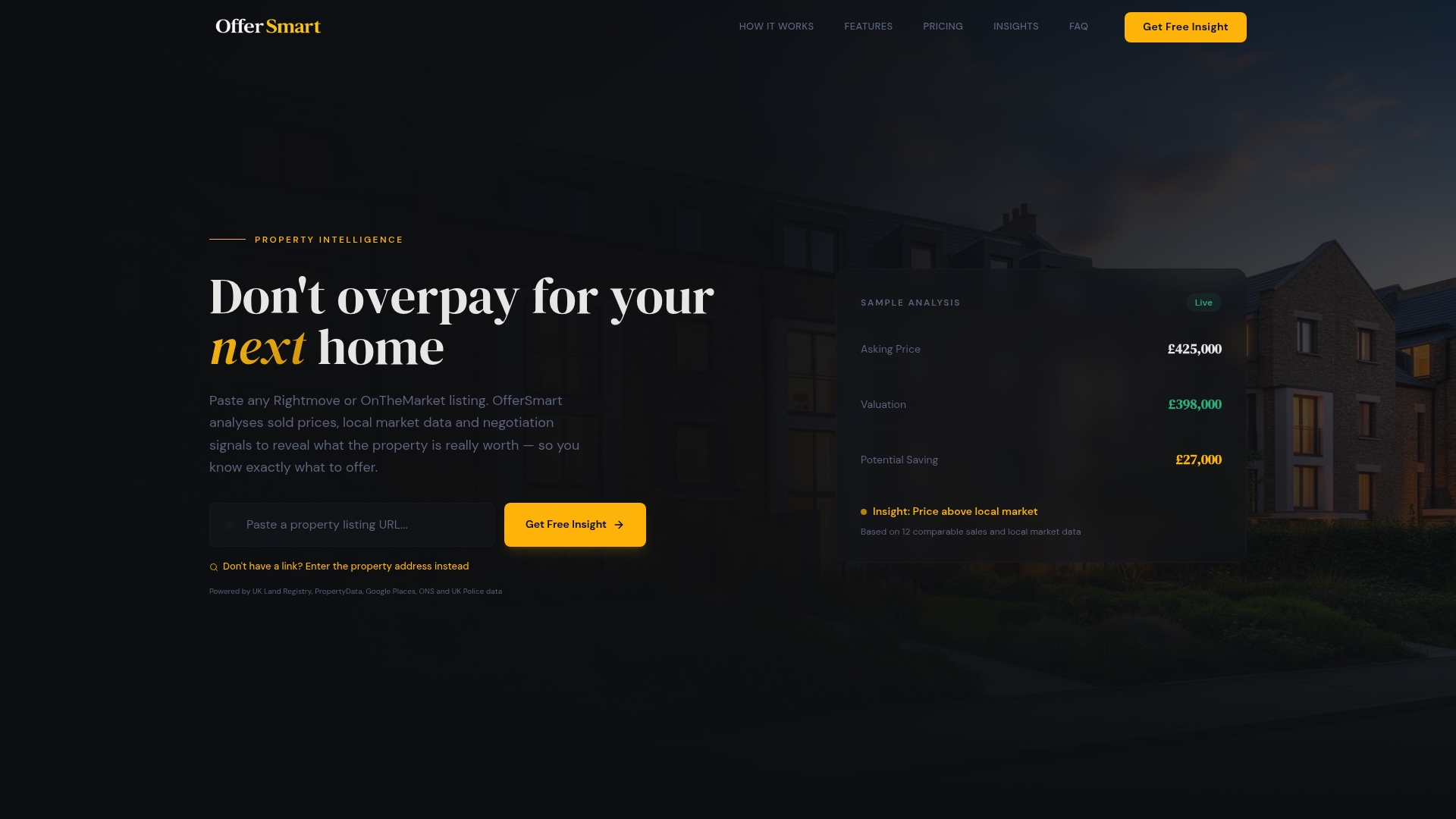

Take the next step with Offer Smart

Ready to buy smart? Here's where to get tailored support.

The workflow in this guide gives you the framework. Offer Smart gives you the data to execute it with precision. When you enter a property address or paste a listing link, the Offer Smart home buying platform instantly analyzes recent comparable sales, calculates what you should realistically offer, and surfaces neighborhood insights including crime risk, flood exposure, school ratings, and lifestyle factors.

For investors, it goes further: rental value estimates, projected ROI, and a 5-year value forecast give you a complete financial picture before you commit. A built-in mortgage calculator and running cost estimates mean no hidden surprises after closing. Whether you are buying your first home or adding to a portfolio, Offer Smart replaces guesswork with clarity so every step of your workflow is backed by real evidence.

Frequently asked questions

What is the most important step in the home buying workflow?

Getting pre-approved for a mortgage is the foundation, as it defines your real budget and accelerates your search. Down payment and affordability concerns top the list for renters considering ownership, making early financial clarity essential.

How can I avoid overpaying on my first home?

Compare recent comparable sales, set a firm budget ceiling, and use data-driven tools to validate your offer price before submitting. Careful, data-driven approaches consistently lead to higher buyer satisfaction and fewer post-purchase regrets.

What's a common regret among recent homeowners?

Underbudgeting for maintenance and unexpected repairs is the most frequently cited regret. 42% of owners report that maintenance issues they didn't anticipate were their biggest source of post-purchase stress.

How do I know if my home purchase was successful?

Success means your final price aligned with comparable evidence, there were no major post-close surprises, and the home fits your lifestyle and budget long term. 58% of renters rank convenience as a key factor, confirming that success is about more than just the purchase price.