Buying your first home is one of the most significant financial decisions you will ever make, yet many first-time buyers still believe a property survey is optional, unnecessary, or only relevant for older homes. This assumption can be costly. From hidden roof damage to structural movement lurking beneath a freshly painted facade, the risks you cannot see during a viewing are often the most expensive to fix. This guide explains exactly why surveys matter, what they reveal, how to choose the right type, and how to use the findings strategically before you exchange contracts.

Table of Contents

- Why viewing alone isn't enough for first-time buyers

- Hidden risks uncovered: what surveys reveal

- Mortgage valuation vs full survey: key differences explained

- Choosing the right survey level: Level 2 vs Level 3

- When and how to use survey findings as leverage

- An expert perspective: why surveys are still undervalued by first-time buyers

- Upgrade your home buying confidence with Offer Smart

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Surveys reveal hidden risks | Property surveys uncover defects that viewings often miss, protecting your investment from costly surprises. |

| Mortgage valuation is not enough | A lender's valuation checks value, not condition, so first-time buyers need an independent survey for real peace of mind. |

| Choose the right survey | Select Level 2 or Level 3 surveys based on property age and condition for best results and risk management. |

| Survey findings empower buyers | Act on survey results before exchange to renegotiate, request repairs, or reconsider your purchase. |

| Surveys aren’t a guarantee | Due to access limits, some issues may be missed, so treat your survey as a key risk filter, not a perfect safety net. |

Why viewing alone isn't enough for first-time buyers

When you attend a property viewing, you typically have 20 to 30 minutes inside a home. You are assessing the layout, the light, and whether you can picture yourself living there. You are not checking the roof void for moisture ingress, inspecting the party wall for lateral movement, or identifying whether the subsidence crack above the bay window is cosmetic or structural. These are the things that what smart buyers check before making an offer.

A viewing is a first impression. It is not a professional inspection. In the UK, a home survey is valuable for first-time buyers because viewings are limited in scope and a survey provides an independent, professional assessment before you are legally committed, giving you the ability to renegotiate or walk away. Once you exchange contracts, that option largely disappears.

Here is what standard viewings typically cannot tell you:

- Whether the roof coverings are near the end of their serviceable life

- If damp is present behind fitted furniture or under floor coverings

- Whether previous extensions have building regulations approval

- If drainage systems are functioning correctly

- Whether the property has adequate structural support following internal alterations

Think of a due diligence checklist approach used in commercial property transactions. First-time buyers deserve the same level of rigour. Survey findings can empower you to renegotiate a lower price, request repairs before completion, or walk away before incurring legal costs on a property with serious problems. To avoid overpaying, a survey is one of your most practical tools.

"The difference between what you see at a viewing and what a chartered surveyor finds can represent tens of thousands of pounds in remediation costs. Most buyers don't realise this until after completion."

Hidden risks uncovered: what surveys reveal

The most uncomfortable truth about property defects is that they are designed, unintentionally, to stay hidden. Sellers redecorate. Estate agents schedule viewings in good lighting. And buyers, naturally excited, focus on potential rather than problems. A chartered surveyor does the opposite.

A survey helps uncover issues that simply are not obvious during a viewing, including roof defects, damp and water ingress, and structural movement. These issues can lead to expensive remediation work and affect the property's future insurability and saleability. That last point matters more than most buyers appreciate. A property with a history of serious damp or underpinned foundations can be difficult to sell in future or expensive to insure.

Common defects that surveys regularly uncover include:

- Roof defects: Missing or slipped tiles, failed flashings around chimneys, and deteriorated felt beneath roof coverings

- Damp and water ingress: Rising damp at ground level, penetrating damp through external walls, and condensation damage in roof spaces

- Structural movement: Cracking in brickwork, lintel failure above windows and doors, and subsidence in properties on clay soils

- Electrical and drainage concerns: Outdated consumer units flagged for further investigation, and slow or blocked drainage noted for specialist review

- Timber defects: Wet rot in window frames, dry rot in floor voids, and woodworm in older timber elements

Pro Tip: Do not assume that a modern or well-presented property is problem-free. A property built in the 1990s can have roof coverings approaching the end of their life, poorly installed cavity wall insulation causing damp, and conservatories added without adequate structural support. Presentation is not a substitute for inspection.

When you know about a defect before exchanging, you have real leverage. You can use survey findings when offering below asking price and negotiate a price reduction that reflects the actual cost of repairs. That is a very different position from discovering the same problem six months after moving in.

"A survey is not about trying to find reasons not to buy. It is about understanding exactly what you are buying, at what cost, and with what risks attached."

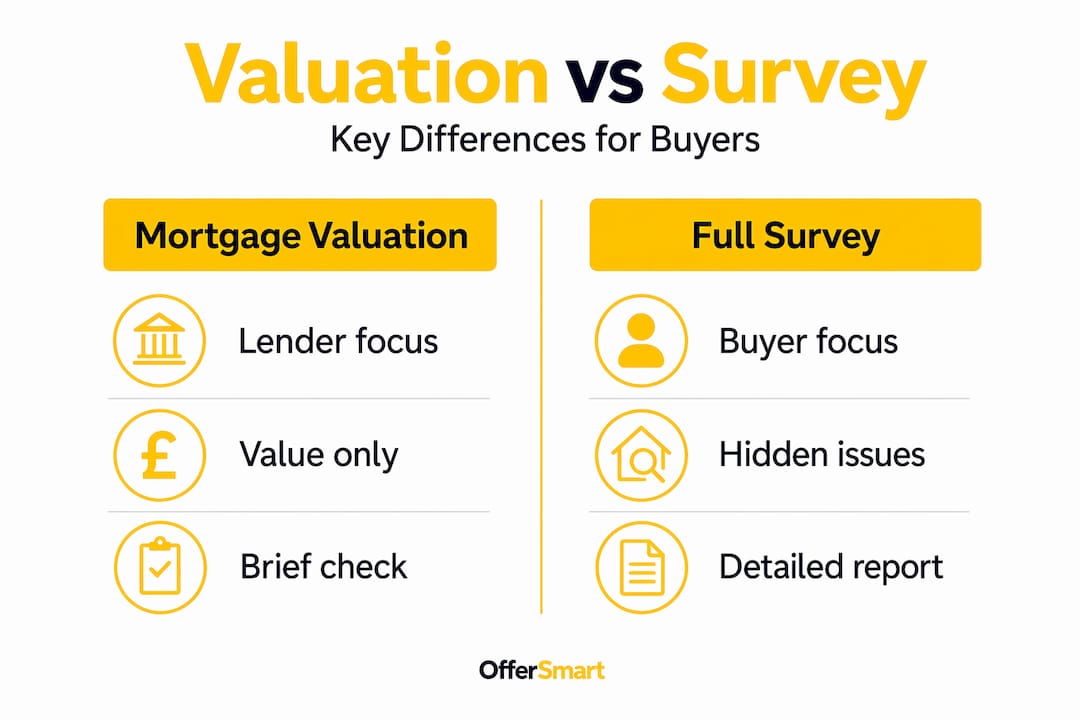

Mortgage valuation vs full survey: key differences explained

This is the area where first-time buyers most commonly misunderstand their position. When your mortgage lender sends a surveyor to assess the property, you might reasonably assume that someone has checked it on your behalf. They have not.

Mortgage lenders typically require a valuation for lending and security purposes, which is not a detailed home inspection for the buyer's benefit. The valuation answers one question: is this property worth at least the amount we are lending? It does not assess the condition of the roof, the presence of damp, or whether the electrical installation is safe. It is carried out for the lender, not for you.

Here is a clear comparison of what each type of report actually covers:

| Feature | Mortgage valuation | Level 2 HomeBuyer report | Level 3 building survey |

|---|---|---|---|

| Purpose | Lender's security | Buyer's condition check | Buyer's detailed inspection |

| Condition assessment | Minimal or none | Yes, traffic light rating | Yes, detailed narrative |

| Roof inspection | External only (sometimes) | Yes | Yes, with access where possible |

| Damp checks | Not included | Yes | Yes, with moisture readings |

| Structural assessment | Basic | Moderate | Thorough |

| Reinstatement cost estimate | Sometimes | Yes | Yes |

| Buyer protection | No | Yes | Yes |

Once your offer is accepted, the steps to commission your own survey are straightforward:

- Confirm your offer has been accepted in writing by the estate agent.

- Ask your mortgage broker or solicitor for RICS (Royal Institution of Chartered Surveyors) accredited surveyor recommendations.

- Contact two or three surveyors for quotes, providing the property address and details.

- Book the survey promptly as delays can affect your timeline.

- Receive the report, read it carefully, and discuss findings with your solicitor before proceeding.

Understanding the mortgage calculator and calculating your offer accurately are important steps, but they need to be paired with survey knowledge to give you a complete financial picture.

Choosing the right survey level: Level 2 vs Level 3

Not all surveys are equal, and choosing the wrong level for your property type is a common and costly mistake. The two main options for residential buyers in the UK are the Level 2 HomeBuyer Report and the Level 3 Building Survey.

Which survey level to commission matters: Level 2 is a common mid-level choice for many conventional properties, while Level 3 is more thorough and better suited to older, unusual, or poor-condition properties and higher-risk situations.

| Survey level | Best suited for | Key limitation |

|---|---|---|

| Level 2 HomeBuyer report | Properties built post-1930 in reasonable condition | Less detail on older or complex structures |

| Level 3 Building survey | Pre-1930 properties, unusual construction, poor condition | Higher cost, longer turnaround |

It is also worth understanding what surveys cannot do. Surveys are constrained by access and visual limitations and are not guaranteed to detect concealed or inaccessible problems. A surveyor cannot lift fitted flooring, open up wall cavities, or inspect behind kitchen units. Treat the survey report as a risk screen. If the surveyor flags a concern about the roof void but cannot fully access it, commission a specialist roofing contractor to inspect further before you proceed.

Key factors to help you decide between survey levels:

- Age of property: Anything pre-1930 almost always warrants a Level 3 survey

- Construction type: Timber frame, stone construction, or thatched roofing requires greater scrutiny

- Visible condition: Obvious signs of age, repair work, or previous alterations suggest a Level 3

- Location and risk: Properties near trees on clay soils carry higher subsidence risk

- Price: The higher the purchase price, the more a thorough survey is justified

Pro Tip: The cost difference between a Level 2 and Level 3 survey is typically £200 to £400. On a property worth £300,000, that additional spend is negligible compared to the risk of missing a significant structural issue. Always use local property data alongside your survey to build a full picture, and consult a buyer advisory service if you are unsure how to interpret findings.

When and how to use survey findings as leverage

The timing of your survey is as important as the type you choose. Commission it too early and you may waste money if the deal falls through for legal reasons. Leave it too late and you risk running out of time before exchange.

The timing and leverage work together: commissioning a survey after the offer is accepted but before exchange allows you to react to findings while options still exist. This is your window to renegotiate, request repairs, or reconsider altogether.

Follow this sequence to maximise your position:

- Offer accepted: Instruct your solicitor and commission a surveyor simultaneously. Do not wait.

- Survey completed: Read the full report, not just the summary. Pay attention to all items rated amber or red.

- Assess the findings: Identify issues that require immediate action versus those that are manageable maintenance items.

- Get specialist quotes: For significant defects, obtain written quotes from qualified contractors before renegotiating.

- Negotiate with evidence: Use the quotes to support a price reduction request or ask the seller to carry out remediation before completion.

- Make a clear decision: Proceed, renegotiate, or withdraw before exchange. After exchange, your legal commitment is binding.

Pro Tip: Present your renegotiation as factual and evidence-based, not emotional. Share the surveyor's report excerpt alongside the contractor's written quote. Sellers and agents respond to documented costs, not general concerns. Also factor in stamp duty calculator figures when assessing whether a renegotiated price still makes financial sense overall.

One important point many first-time buyers overlook: withdrawing after a survey, before exchange, is entirely acceptable and legally clean. You may lose your survey fee and some solicitor costs, but these are far less than the financial damage of proceeding with a property that has serious structural or damp issues.

An expert perspective: why surveys are still undervalued by first-time buyers

Here is the honest reality. Most first-time buyers who skip a survey do so for one of three reasons: they believe the property looks fine, they trust the estate agent's reassurance, or they are trying to reduce upfront costs at an already expensive stage. Each of these is understandable. None of them is a sound reason to proceed without a survey.

Even relatively new or good-looking properties can hide issues that only become apparent after weather exposure or occupancy. Conditions that seemed acceptable during a dry summer viewing can reveal significant damp problems in winter. A chartered surveyor has the training and equipment to identify warning signs that no amount of careful looking by an untrained eye will catch.

The objection we hear most often is that surveys are not legally required, so some buyers feel they can rely on viewings or the lender's valuation. But mortgage valuations are explicitly for lender protection rather than detailed buyer due diligence. Relying on a lender's valuation for your own protection is like relying on a shop's security guard to protect your personal belongings. They serve different interests.

Our view at Offer Smart is simple. A survey is not paperwork. It is buyer protection. It is the one step in the purchase process that exists entirely in your interest, carried out by a professional who has no stake in whether the sale proceeds. Understanding what smart buyers check before committing is foundational to every confident purchase decision, and a survey sits at the centre of that process.

Do not treat the cost of a survey as an added burden. Treat it as the most targeted due diligence spend available to you in the entire buying process.

Upgrade your home buying confidence with Offer Smart

A property survey tells you what the building is hiding. Offer Smart tells you what the market is hiding.

Understanding surveys is just one part of making a confident first purchase. You also need to know whether the asking price is realistic, what comparable properties on the same street have sold for, and what your true monthly costs will be. Offer Smart provides all of this in one place. Use the mortgage calculator to model your repayments, explore property calculators to stress-test your offer, and let Offer Smart give you a data-driven view of what you should realistically pay. Pair that with a professional survey, and you are negotiating from genuine knowledge.

Frequently asked questions

Are property surveys mandatory for first-time buyers in the UK?

No, surveys are not legally required, but skipping one leaves you exposed to serious undiscovered defects and potentially significant repair costs after completion.

What defects are most commonly missed when buyers skip a survey?

Roof defects, damp, water ingress, and structural movement are routinely missed by buyers who rely on viewings alone and can seriously affect insurability and future resale value.

Is a mortgage valuation the same as a property survey?

No, a mortgage valuation assesses value for the lender's security purposes only and does not inspect property condition or identify defects for the buyer's benefit.

Which survey level should I choose for my first home?

Level 2 is suitable for conventional, newer homes in reasonable condition, while Level 3 Building Survey is recommended for properties over 50 years old, unusual construction types, or those in poor condition.

Can a survey find all possible problems in a property?

No, surveys are limited by access and visibility and cannot inspect concealed areas, meaning significant findings may prompt specialist follow-up investigations rather than providing a complete guarantee.