Losing your dream home to another buyer because your offer wasn't structured correctly is one of the most frustrating experiences in real estate. You found the right property, you felt the connection, and then someone else's paperwork beat yours to the finish line. That scenario plays out constantly for first-time buyers who focus all their energy on finding the home but not enough on how to secure it. This guide walks you through every step of preparing and submitting a competitive offer, so you move forward with clarity, confidence, and a real shot at getting the keys.

Table of Contents

- What to gather before you make an offer

- Step-by-step instructions: How to prepare and submit your offer

- Making your offer stand out: Contingencies, deposits, and terms

- Troubleshooting: Common mistakes and how to avoid them

- What most first-time buyers miss when preparing an offer

- Take the next step with Offer Smart's tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Get pre-approved first | Mortgage pre-approval and proof of funds make your offer credible to sellers. |

| Follow a clear sequence | Successful offers use a step-by-step process covering price, terms, contingencies, and negotiation. |

| Customize for competitiveness | Adjust contingencies and terms to match seller priorities and market conditions. |

| Avoid common pitfalls | Avoid skipping documentation, missing deadlines, or offering too little earnest money. |

What to gather before you make an offer

Before you write a single number on an offer form, your financial and documentation foundation needs to be solid. Sellers and their agents make quick judgments about buyer credibility. An incomplete or unverified package signals risk, and sellers in competitive markets will simply move on.

The most critical item is your mortgage pre-approval letter. This is not the same as pre-qualification. Pre-approval uses verified financial information, including income, employment, assets, and credit history, while pre-qualification is an informal estimate based on self-reported numbers. In high-demand markets, pre-qualification carries very little weight with sellers. Pre-approval tells them you've been vetted by a lender and can actually close.

Beyond the pre-approval letter, you need to confirm that your cash reserves are in order. Mortgage preapproval is just the start. You also need readily available funds for the down payment, earnest money deposit, and closing costs. These are three separate financial requirements, and buyers often underestimate the total cash needed at the offer stage. Closing costs alone typically run between 2% and 5% of the loan amount.

Here's a quick checklist of what to gather before you submit:

- Mortgage pre-approval letter (dated within 60 to 90 days)

- Proof of funds for down payment and earnest money

- Bank statements (typically the last two to three months)

- Contact details for your real estate agent and mortgage lender

- Government-issued photo ID

- Any gift letter documentation if part of your funds are gifted

Understanding what to check before making an offer goes beyond finances. You should also review the property's listing history, days on market, and any recent price reductions before sitting down to write your offer.

| Document | Why it matters |

|---|---|

| Mortgage pre-approval letter | Proves you're a credible, vetted buyer |

| Proof of funds | Confirms you can cover down payment and deposits |

| Bank statements | Verifies financial stability to the seller |

| Agent contact details | Speeds up communication during negotiations |

| Photo ID | Required for legal documentation |

| Gift letter (if applicable) | Clarifies the source of any gifted funds |

Pro Tip: Organize all your documents into a single digital folder before you start touring homes seriously. When the right property appears, you'll be ready to act within hours, not days.

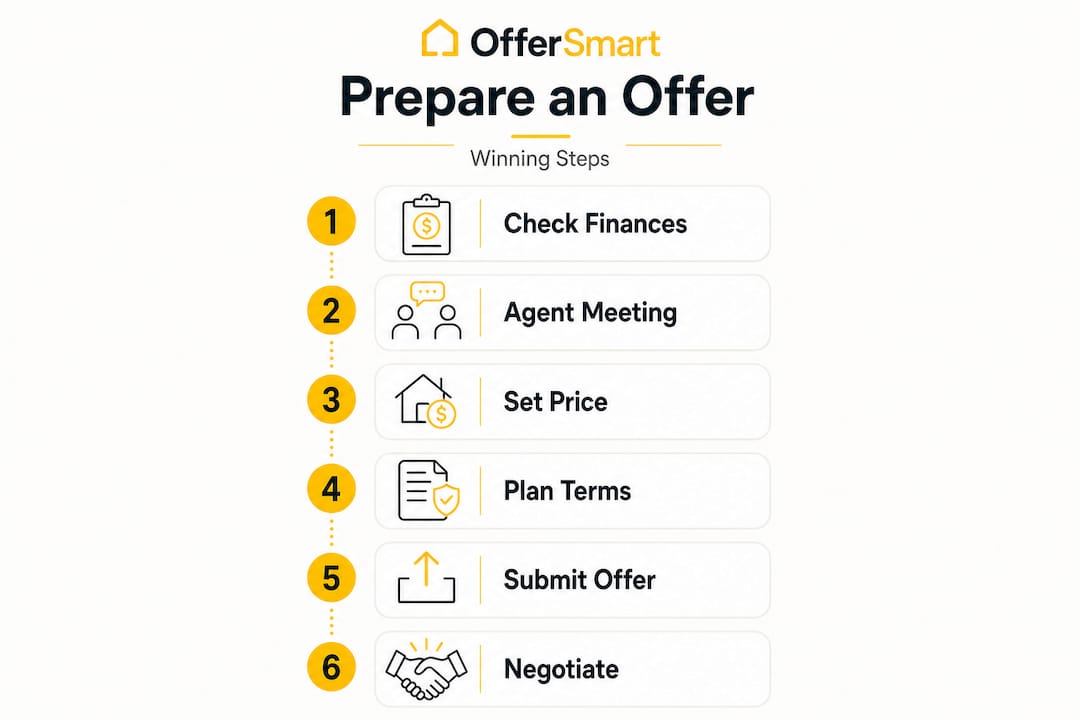

Step-by-step instructions: How to prepare and submit your offer

Once all essentials are gathered, here's exactly how to move through the offer process step by step.

Step 1: Confirm your finances one more time. Before anything else, speak with your lender to confirm your pre-approval is current and your loan amount still aligns with the property's price range. Markets move fast, and interest rate changes can affect your purchasing power between when you started looking and when you found the right home.

Step 2: Discuss strategy with your real estate agent. Your agent is your most valuable resource here. They can pull comparable sales (often called "comps") in the neighborhood, tell you how long the home has been listed, and advise whether the market favors buyers or sellers right now. This conversation shapes every decision that follows.

Step 3: Set your offer price and earnest money amount. Use recent local sales data to anchor your price. Deciding your offer price is one of the most consequential steps in the process. Going too low risks insulting the seller and losing the home. Going too high means you may overpay. Pair your price decision with an earnest money deposit that signals seriousness.

Step 4: Choose your contingencies. Contingencies are conditions that must be met for the sale to proceed. Common ones include inspection, appraisal, and financing contingencies. Each one protects you, but each one also adds complexity from the seller's perspective. Choose carefully based on your risk tolerance and market conditions.

Step 5: Prepare the written offer. Your agent will draft the formal purchase agreement. Review every line. Confirm the offer price, earnest money amount, contingencies, proposed closing date, and any personal property you're requesting (appliances, fixtures, etc.). Errors or missing information at this stage can slow the process or raise red flags.

Step 6: Submit the offer. Your agent delivers the offer to the listing agent, usually with a deadline for the seller to respond. In competitive markets, response windows can be as short as 24 hours. Make sure your agent is reachable and ready to negotiate quickly.

Step 7: Negotiate or move toward closing. Sellers may accept, reject, or counter your offer. A counter offer is not a rejection. It's an invitation to continue the conversation. Stay calm, review any counter carefully with your agent, and respond within the specified timeframe.

Analyzing local data for your offer is critical at steps three and four. The more precisely you understand what comparable homes have sold for, the more confident and accurate your offer will be.

| Feature | Standard offer | Competitive offer |

|---|---|---|

| Financing | Pre-qualification letter | Verified pre-approval letter |

| Earnest money | 1% of purchase price | 2 to 3% of purchase price |

| Contingencies | Multiple, loosely defined | Selective, clearly stated |

| Closing timeline | Flexible or unspecified | Specific and seller-friendly |

| Documentation | Partial or delayed | Complete and submitted promptly |

| Personal letter | Not included | Optional but thoughtful |

Pro Tip: Make your proposed closing date align with what the seller actually wants. Ask your agent to find out the seller's preferred timeline before you submit. Matching their needs on timing, even if your price isn't the absolute highest, can be the deciding factor.

Making your offer stand out: Contingencies, deposits, and terms

As you structure your formal offer, these elements can differentiate you from other buyers.

Earnest money is the good-faith deposit you put down when your offer is accepted. It shows the seller you're serious and financially committed. Earnest money is typically around 3% of the purchase price in many markets, though it can range from 1% to 3% depending on your location and the competitiveness of the situation. On a $400,000 home, that's $4,000 to $12,000 held in escrow until closing. If you walk away without a valid contingency reason, you risk losing that deposit.

Common contingencies to understand:

- Inspection contingency: Gives you the right to have the home professionally inspected and to negotiate repairs or back out if major issues are found

- Appraisal contingency: Protects you if the home appraises below your offer price, allowing you to renegotiate or exit

- Financing contingency: Lets you exit the deal without penalty if your mortgage falls through

- Sale of current home contingency: Makes your purchase dependent on selling your existing property first (this one can weaken your offer significantly in competitive markets)

Understanding how estate agents assess offers helps you see the transaction from the seller's side. Sellers want certainty. The fewer conditions attached to your offer, the more attractive it looks. That doesn't mean you should waive every protection, but it does mean you should be intentional about which ones you include.

"In a multiple-offer situation, the best offer is not always the highest price. Sellers consider terms, timelines, and the overall certainty of the deal." — NAR multiple offers guide

Waiving contingencies carries real risk. Skipping an inspection contingency means you accept the home as-is, including any hidden defects. Only consider this if you've done thorough due diligence and understand the property's condition. Guidance on avoiding overpaying is especially relevant here, since waiving an appraisal contingency can leave you on the hook for the gap between your offer price and the appraised value.

Troubleshooting: Common mistakes and how to avoid them

Even great offers can fail. Let's explore potential hazards to watch for.

The most common mistake is submitting an offer without a proper pre-approval letter. Some buyers still use pre-qualification letters, not realizing that sellers and their agents see these as insufficient. Mortgage preapproval with verified financial information is the minimum standard for a credible offer in most markets today.

Other frequent mistakes include:

- Insufficient funds: Buyers sometimes forget to account for closing costs on top of the down payment and earnest money. Calculate your total cash requirement before submitting.

- Missing deadlines: Offers have expiration times. Failing to respond to a counter offer within the window can kill the deal entirely.

- Unclear or conflicting contingencies: Vague language in contingency clauses creates disputes. Make sure every condition is written clearly with specific timeframes.

- Lowball offers without justification: Offering significantly below asking price without comparable sales data to back it up can offend sellers and close the door on negotiation.

- Skipping the agent's advice: First-time buyers sometimes try to manage the process alone to save on commission. This often leads to costly errors in documentation and negotiation.

- Not reading the full purchase agreement: Every line matters. Missed clauses about inclusions, exclusions, or timelines can cause problems at closing.

Revisiting essential checks before your offer is a smart habit before you submit anything. A quick review of your documentation, finances, and the property itself can catch issues before they become expensive problems.

Pro Tip: Create a personal submission checklist and go through it the night before you submit your offer. Confirm your pre-approval letter is current, your proof of funds is attached, your contingency language is clear, and your agent has all the contact details they need to respond quickly.

What most first-time buyers miss when preparing an offer

Here's the honest truth that most guides won't tell you directly: the majority of first-time buyers spend 90% of their mental energy on the offer price and almost none on the quality of their execution.

Price matters. But in many situations, especially when multiple buyers are competing for the same property, the winning offer isn't the highest one. It's the most complete, most credible, and fastest one. Sellers are not just evaluating a number. They're evaluating whether they believe you can actually close.

Speed is a competitive advantage that most buyers underestimate. When you're already pre-approved, have your documents organized, and have done your research on comparable sales, you can submit a strong offer within hours of seeing a property. Buyers who need three days to gather paperwork lose homes to buyers who were ready on day one.

There's also a professionalism factor that goes unspoken. An offer package that's complete, clearly written, and submitted with a courteous cover note from your agent creates a different impression than a rushed, incomplete submission. Sellers and listing agents remember how a buyer's team communicates. That perception can influence how they respond to a counter offer or whether they choose your offer over a slightly higher but messier one.

Flexibility on non-price terms is another underused tool. If a seller needs to close in 45 days because they're buying another home, matching that timeline exactly can be worth more to them than an extra $5,000 on the offer price. Ask your agent to find out what the seller actually needs. Then give it to them if you can.

Reviewing offer amount strategies is important, but pair that research with a commitment to execution quality. The strongest offers are more than just numbers. They're about certainty, speed, and trust.

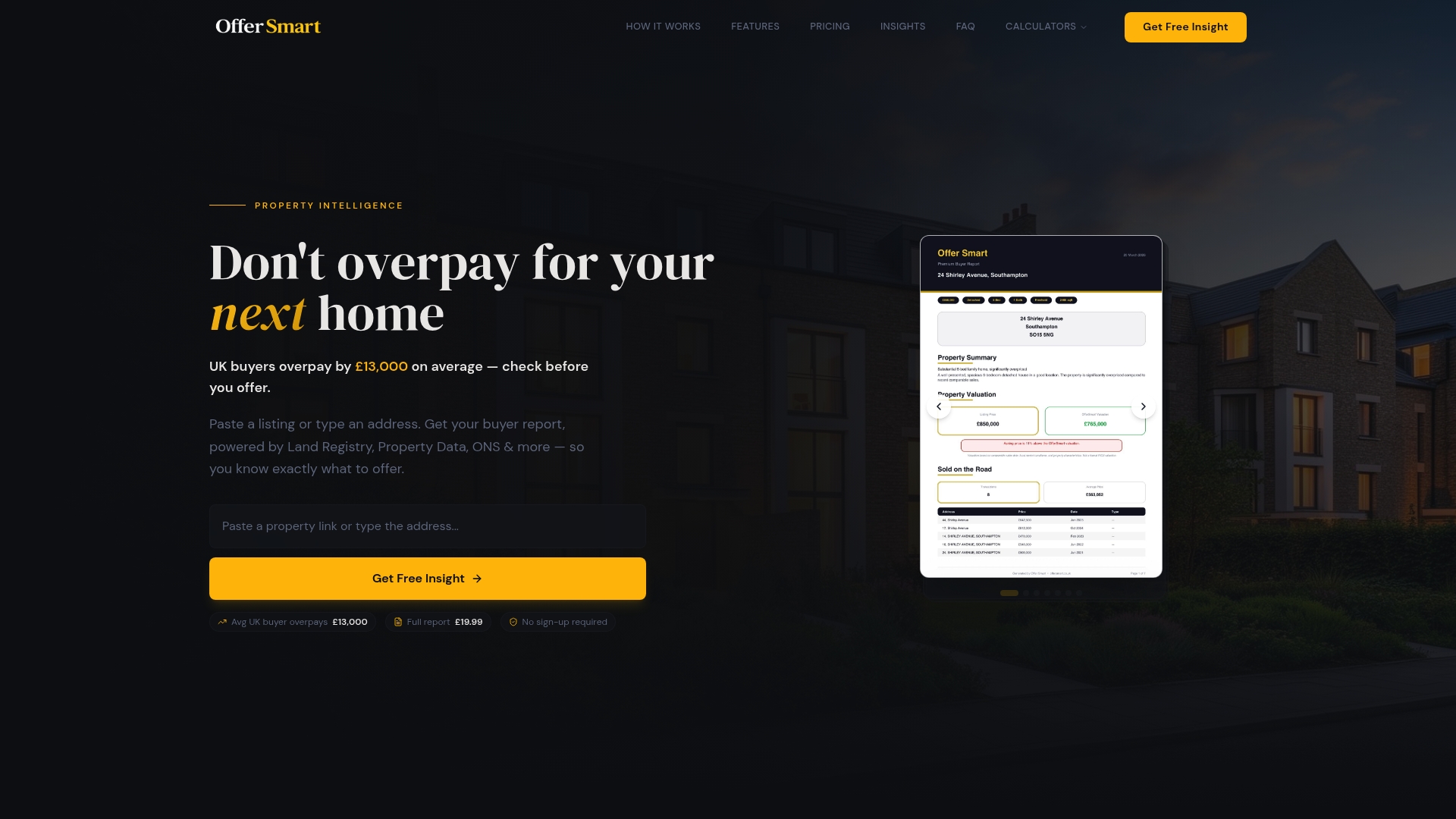

Take the next step with Offer Smart's tools

You now have a clear framework for preparing and submitting a competitive offer. The next step is putting real numbers behind your strategy before you hit submit.

Offer Smart gives you instant access to comparable local sales, a 5-year value forecast, and area insights including crime risk, flood risk, and lifestyle data so you know exactly what a property is worth before you write your offer. Use the mortgage calculator to confirm your monthly payments at different offer prices, and explore the full suite of offer calculators to model your total costs, estimated ROI, and running expenses. Enter a property address or paste a listing link, and Offer Smart gives you the data-driven clarity to move forward with confidence and avoid overpaying.

Frequently asked questions

What documents do I need before making an offer on a house?

You'll need a mortgage pre-approval letter and proof of funds for the down payment and earnest money, along with recent bank statements and a valid photo ID.

How much earnest money should I put down?

Earnest money is typically between 1% and 3% of the purchase price, with 3% being common in many competitive markets.

What is the difference between pre-qualification and pre-approval?

Pre-approval uses verified financial information such as income, employment, and credit history, while pre-qualification is an informal estimate based on self-reported data and carries far less weight with sellers.

Can I negotiate terms other than the offer price?

Yes. Sellers consider more than just price. Contingencies, closing timelines, earnest money amounts, and included appliances or fixtures are all negotiable and can make your offer more appealing without raising your price.