Paying too much for a property feels like a minor miscalculation in the heat of a competitive market. It rarely is. Understanding why overpaying on a house matters is not about dampening excitement. It is about protecting yourself from consequences that unfold quietly over years: a lender who won't fund the full price, a stamp duty bill that jumps by thousands at a single threshold, or a property you cannot sell without taking a loss. This guide covers every layer of that risk, from the moment your offer is accepted to the decade that follows.

Table of Contents

- Key takeaways

- Why overpaying on a house matters to your mortgage

- Stamp duty: the cost that jumps without warning

- Long-term risks of overpaying for property

- How to avoid overpaying on a house

- My view: data beats the heat of the moment

- Make your next offer with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Lender valuations can block completion | If your mortgage lender values the property below your agreed price, you must cover the gap from your own funds or renegotiate. |

| Stamp duty thresholds create cliff edges | Crossing the £500,000 mark as a first-time buyer can trigger a tax jump of over £15,000 on a single pound of difference. |

| Hidden ongoing costs add up fast | Maintenance, insurance, and utility variability mean the true cost of a property extends well beyond the purchase price. |

| Comparable sales are your strongest tool | Recent local sales data is what wins valuation appeals and informs credible offers. Opinions carry no weight. |

| Emotional bidding has a real price | Buyers who overpay due to sentiment often only recognise the financial damage months or years later. |

Why overpaying on a house matters to your mortgage

Most buyers assume that once a seller accepts their offer, the money side is settled. It is not. Your mortgage lender will instruct their own surveyor to value the property independently, and that valuation often tells a very different story from the agreed price.

What a down valuation actually means

A down valuation occurs when the lender values the property below what you have agreed to pay. Lenders do not care what you feel the property is worth or what the seller insists it fetches. They care about what they could recover if you defaulted and they had to sell. That conservative, security-focused view can lag behind fast-moving local markets, particularly where limited comparable evidence exists.

When this happens, your mortgage offer may fall short of the agreed purchase price. You are then left with four options:

- Cover the funding gap from your own savings or deposit

- Renegotiate the purchase price with the seller using the valuation as leverage

- Formally appeal the down valuation with supporting comparable sales evidence

- Walk away from the transaction entirely

None of these options are comfortable, and all of them take time. If you are in a chain, time is exactly what you do not have.

How to challenge a down valuation

Appealing a down valuation is possible, but only if you have substance behind the challenge. Down valuation appeals succeed when buyers can point to recent sales of genuinely comparable properties on the same road or in the immediate vicinity, ideally completed within the past three to six months. Opinions, personal attachment, or the estate agent's enthusiasm are not evidence.

Pro Tip: Build an evidence pack before you make an offer. Print or save sold prices for three to five comparable properties nearby. If a down valuation arrives, you can respond within days rather than scrambling for data under pressure.

Preparing this evidence pack early also sharpens your own view of what the property is genuinely worth, which is precisely what smart buyers check before committing to any figure.

Stamp duty: the cost that jumps without warning

Stamp duty land tax is paid on top of the purchase price. For most buyers, it registers as a line item on the completion statement. For buyers close to key thresholds, it can be the single most expensive mistake of the entire transaction.

How the thresholds work in England and Northern Ireland

The SDLT system is tiered, meaning you pay different rates on different portions of the price. First-time buyers benefit from relief, but only up to a point. First-time buyers pay 0% on the first £300,000 and 5% on the portion between £300,001 and £500,000. Cross £500,000 and that relief disappears entirely. The full standard rates apply from the first pound.

To illustrate the scale of this cliff edge:

| Purchase price | SDLT for first-time buyer | SDLT difference |

|---|---|---|

| £499,999 | £9,999 | Baseline |

| £500,001 | £25,000 | +£15,001 |

| £525,000 | £26,250 | +£16,251 |

A single pound above that threshold costs you over £15,000. This is not a rounding error. It is a structural feature of the tax system that rewards buyers who model their offers carefully before submitting them.

Beyond the threshold mechanics, SDLT must be paid and a return filed within 14 days of completion. Your conveyancer will usually handle the payment, but you must have the funds available. Treating stamp duty as an afterthought rather than part of your affordability model is a common and costly mistake.

Use the Offersmart stamp duty calculator to model your liability before you make any offer, not after.

Long-term risks of overpaying for property

The financial implications of overpaying do not stop at completion. Some of the most significant consequences of overpaying for a home take months or years to become visible, by which point your options are narrower.

When life changes and the property no longer fits

Overpaying can reduce future flexibility in ways that buyers rarely anticipate. A property purchased at a premium leaves you with less equity. If you need to relocate for work, upsize for a growing family, or sell during a market dip, you may find yourself unable to achieve a price that covers what you paid. You are effectively locked in until the market catches up, if it does at all.

The long-term effects of overpaying are compounded by ongoing costs that vary more than buyers expect:

- Maintenance and repairs: Older properties or those with structural issues carry unpredictable costs. A premium paid for perceived charm can quickly be absorbed by a boiler replacement or roof repair.

- Buildings and contents insurance: Premiums reflect rebuild cost and location risk, including flood risk. A property in a high-risk area may cost significantly more to insure year on year.

- Service charges and ground rent: For leasehold properties, these can rise substantially over time and affect both affordability and resale value.

- Utility costs: Large period properties with poor insulation carry far higher running costs than their initial appeal suggests.

The resale and rental demand problem

Overpaying in real estate creates a resale ceiling that buyers rarely think about at the point of purchase. If you have paid above what comparable properties achieved, the next buyer has no obligation to match your price. They will look at the same comparable sales data and offer accordingly.

For investors, the impact of overpaying on home value is even more direct. Rental yields are calculated on actual market rents, not on what you paid. Overpay for a property and your yield compresses immediately, affecting your return on investment from day one.

Pro Tip: Before making an offer, look at the rental value of similar properties in the same street. If the numbers do not produce a yield you are comfortable with, that is useful information whether you are buying to let or simply trying to understand the property's true market position.

How to avoid overpaying on a house

Avoiding overpayment is less about being cautious and more about being prepared. Here is a practical approach that UK buyers can apply directly.

-

Gather recent comparable sales before you offer. Use Land Registry data and local sold prices to understand what similar properties on the same road have actually achieved, not just what they were listed for. This is the foundation of any credible offer. The Offersmart guide to using local property data walks through this methodology clearly.

-

Model your stamp duty liability at every price point you are considering. If you are close to a threshold, a small reduction in your offer could save you more than the discount itself. Run the numbers before you negotiate.

-

Understand how estate agents value properties. Estate agents price to attract interest, not to reflect the precise midpoint of market value. Knowing how estate agents value properties helps you separate the listing strategy from the actual evidence.

-

Decide your offer based on evidence, not competition. In a bidding situation, the impulse to simply outbid the competition is understandable. However, winning a bid is not the same as making a good decision. Set a ceiling based on comparable data and hold to it.

-

Factor in mortgage overpayment capacity as part of affordability. If you want to pay down your mortgage faster, note that lenders typically allow overpayments of up to 10% of the outstanding balance per year without penalty. Exceeding this can trigger fees. Build this into your financial planning from the start.

-

Use a mortgage calculator to stress-test affordability. Model what happens to your monthly payments if rates rise or your income changes. The Offersmart mortgage calculator lets you run these scenarios before you commit.

Pro Tip: If you are unsure whether to offer below the asking price, read Offersmart's breakdown of how much below asking price buyers typically offer in different market conditions. The answer varies by area and market temperature, and knowing it before you negotiate gives you a real advantage.

Understanding how to calculate your offer on a UK property using comparable sales removes the guesswork entirely and replaces it with a figure you can defend.

My view: data beats the heat of the moment

I have watched buyers win bidding wars and immediately question whether they did the right thing. The energy of a competitive offer situation is real. There is genuine pressure, and the fear of losing a property you have spent weeks viewing is not irrational. But I have also seen what happens when that emotional momentum carries someone past the point where the numbers make sense.

In my experience, the buyers who regret their decisions share one thing in common: they prioritised winning over understanding. They confused the estate agent's enthusiasm for market evidence. They assumed the lender would simply follow their logic. And they discovered, sometimes years later, that the mortgage rate versus investment return calculation they skipped at the start was actually the most important one they could have done.

The buyers I have seen fare best are those who walked into negotiations with comparable sales printed out, stamp duty modelled at multiple price points, and a clear ceiling based on evidence rather than emotion. They were not the buyers who never lost a property. They were the buyers who never overpaid for one.

Data-driven decisions and personal circumstances are not opposites. You can love a property and still verify what it is worth. That combination is where confident, sound decisions come from.

— Rhys

Make your next offer with confidence

Overpaying is often preventable. You just need the right information before you make your move.

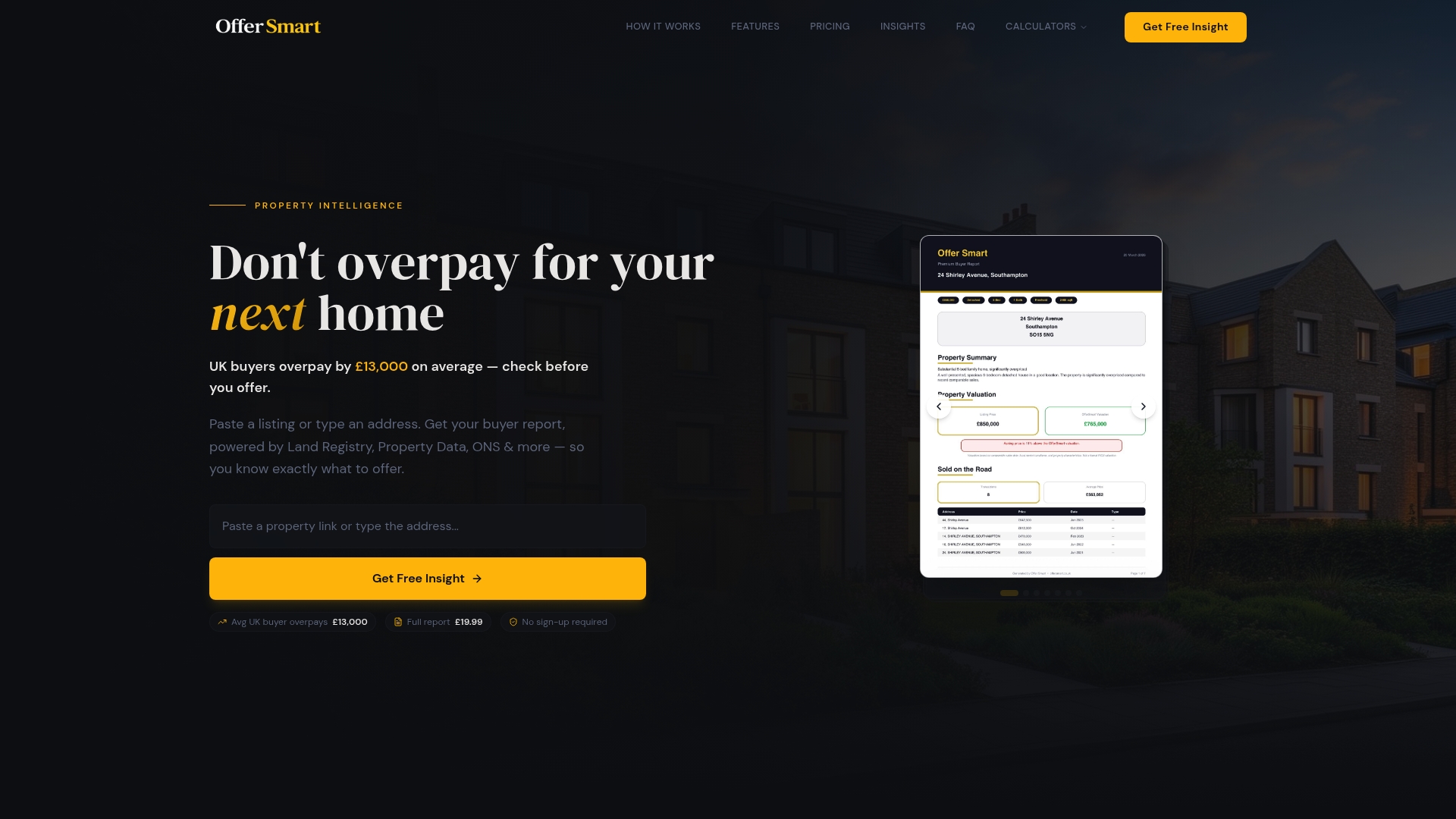

Offersmart gives you an instant property analysis the moment you enter an address or paste a listing link. It compares recent local sales, flags flood and crime risk, estimates rental yield and ROI for investors, and models your stamp duty and mortgage costs in one place. You see what the property is genuinely worth before you put a number on the table. Visit the Offersmart property calculators to model your offer, stamp duty, and mortgage costs before your next viewing. No guesswork. No surprises at completion.

FAQ

What happens if I overpay and my lender down-values the property?

If your lender's valuation comes in below your agreed purchase price, you will need to cover the shortfall from your own funds, renegotiate with the seller, or appeal the valuation with comparable sales evidence. Without action, the transaction is at risk of collapsing.

Can overpaying on a house affect my stamp duty bill?

Yes, significantly. Crossing certain thresholds, such as the £500,000 first-time buyer relief limit, can increase your SDLT liability by over £15,000 on a price difference of just one pound. Modelling stamp duty before you negotiate is not optional.

How do I know if I am overpaying for a property?

Compare your intended offer against recent sold prices for similar properties on the same road or in the immediate area, using Land Registry data. If your figure sits materially above those comparables without a clear justification, you are likely overpaying.

Is it bad to overpay for property in a rising market?

It carries real risk even in rising markets. A lender's conservative valuation may still fall short of your price, your stamp duty exposure remains unchanged, and if the market cools before you need to sell, you could find your equity eroded. Market conditions change; the price you paid does not.

Should I negotiate the home price even in a competitive market?

Yes. Negotiation based on evidence is always worth attempting. Knowing recent comparable sales and understanding market conditions in your area gives you a credible foundation to either negotiate or set a firm ceiling, rather than simply outbidding other buyers without reference to value.