Buying your first home in the UK is one of the most significant financial decisions you will ever make, yet the process is rarely straightforward. Between unfamiliar terminology, competing deadlines, and the sheer number of professionals involved, it is easy to feel lost before you have even viewed a single property. Mistakes at any stage can cost you thousands of pounds or, worse, cause the entire purchase to collapse. This checklist cuts through the noise and gives you a clear, step-by-step guide to every critical stage, so you can move forward with confidence and avoid the pitfalls that catch so many first-time buyers off guard.

Table of Contents

- Assess your readiness and financing options

- Start your search and shortlist smartly

- Making your offer and instructing professionals

- Navigating exchange and completion

- Special cases: Property pitfalls and lender requirements

- What most first-time buyers miss: A perspective on process and pitfalls

- Next steps: Tools and support for first-time buyers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your finances | Secure your mortgage agreement and understand all your buying costs up front. |

| Move quickly after offer | Instruct a solicitor and arrange a property survey as soon as your offer is accepted. |

| Understand key legal stages | Exchange of contracts is when your commitment is binding; completion is when you move in. |

| Watch for property pitfalls | Unusual features or missing documents can stop your mortgage—always clarify before exchange. |

Assess your readiness and financing options

Before you start browsing listings, you need an honest picture of your financial position. Many first-time buyers skip this stage and end up viewing properties they cannot afford, or worse, making offers before their finances are in order. That wastes time and can damage your credibility with estate agents.

Ask yourself these questions first:

- Can you cover a deposit of at least 5% of the purchase price?

- Do you have savings set aside for additional costs beyond the deposit?

- Is your credit score in good shape? Check it via a free service before applying for a mortgage.

- Are you in stable employment, or self-employed with at least two years of accounts?

- Have you factored in stamp duty, solicitor fees, survey costs, and removal expenses?

Deposit requirements in the UK typically range from 5% to 20% of the property price. A larger deposit secures you a better mortgage rate, but a smaller deposit is not necessarily a barrier. The 2025 Mortgage Guarantee Scheme supports mortgages with deposits as low as 5% through participating lenders, available across the UK from July 2025. This is particularly relevant if you are buying in an area where property prices have outpaced your savings.

Statistic: Stamp duty thresholds changed in April 2025. First-time buyers now pay stamp duty on properties above £300,000, with a 5% rate applying between £300,001 and £500,000. Budget for this early.

Beyond the deposit, you need to budget realistically for:

- Solicitor or conveyancer fees: typically £1,000 to £2,500

- Survey costs: between £400 and £1,500 depending on survey type

- Mortgage arrangement fees: often £500 to £2,000, sometimes added to the loan

- Buildings insurance: required from the date of exchange, not completion

Pro Tip: Obtain an Agreement in Principle (AIP) from a lender before you start viewing properties. An AIP confirms how much a lender is likely to offer you, based on a soft credit check. It signals to estate agents that you are a serious buyer and can give you an edge in competitive markets. It is not a guarantee, but it is a powerful credibility tool. Also read up on avoiding overpaying for a house before you set your maximum budget, as many buyers anchor too high from the outset.

Once you have established your readiness and budget, it is time to move into the actual house hunt.

Start your search and shortlist smartly

Most buyers start on the major property portals, and that is a perfectly sensible approach. But searching effectively requires more discipline than simply scrolling through listings. You need clear criteria before you start, otherwise you will waste viewings on properties that do not suit your needs.

When building your shortlist, compare each property against these key factors:

- Location: Proximity to work, schools, transport links, and amenities

- Lease length (for leasehold properties): Anything below 80 years can cause mortgage and resale problems

- Construction type: Standard brick-built properties are easier to mortgage than timber-frame or concrete construction

- Condition: Is it move-in ready, or does it need significant work? Factor renovation costs into your offer

- Service charges and ground rent (leasehold): These can add hundreds or thousands to your annual costs

At viewings, go beyond the surface. Look for damp patches, cracks in walls, signs of subsidence, and the condition of the roof and windows. Check the boiler age and ask when it was last serviced. Look at the electrics. These are the details that property checks before offering can save you from expensive surprises post-purchase.

Understanding how properties are valued is equally important. Estate agents value properties based on comparable sales, local demand, and presentation. Knowing this helps you assess whether an asking price is realistic or inflated.

As a first-time buyers checklist methodology confirms, the sequence runs from searching and viewing to offer acceptance, then into conveyancing, surveys, and mortgage offer. Getting your shortlisting right early saves significant time later.

Pro Tip: Keep a simple spreadsheet tracking each property you view. Note the address, asking price, key pros and cons, and any red flags. When you have viewed six or eight properties, your notes will help you compare objectively rather than relying on memory or emotion.

With a shortlist in hand, the next move is to make an offer and prepare for the crucial legal and survey steps.

Making your offer and instructing professionals

When you find the right property, speed matters. Here is the sequence to follow once your offer is accepted:

- Confirm your mortgage AIP is current and contact your mortgage broker or lender immediately to begin the formal application.

- Instruct a solicitor or licensed conveyancer on the same day your offer is accepted. Delays here are one of the most common reasons purchases fall through.

- Book your survey. Choose the right level: a Condition Report (basic), a HomeBuyer Report (mid-range), or a Building Survey (most thorough, recommended for older or unusual properties).

- Notify your lender so they can arrange their own valuation. This is separate from your survey.

- Keep all parties informed of each other's contact details to avoid communication gaps.

Understanding the difference between the professionals involved is essential:

| Professional | Role | Who pays |

|---|---|---|

| Solicitor or conveyancer | Handles all legal work, searches, and contracts | Buyer |

| Surveyor | Assesses the physical condition of the property | Buyer |

| Mortgage lender | Provides the loan and arranges their own valuation | Buyer (via fees) |

| Estate agent | Represents the seller, not you | Seller |

As the first-time buyers checklist confirms, once an offer is accepted, you need to move quickly into solicitor and conveyancing steps alongside survey and valuation. Stalling at this stage gives other buyers time to make competing offers, and it signals to the seller that you may not be committed.

The survey and lender valuation serve entirely different purposes. The lender's valuation confirms the property is worth what they are lending against. Your survey tells you the actual condition of the building. Never assume the lender's valuation is a clean bill of health for the property.

"Delays between offer acceptance and instructing a solicitor are one of the most avoidable reasons a purchase collapses. Every day of inaction is a day the seller could accept another offer."

Knowing how much to offer on a house before you negotiate is critical. Going in too high costs you money; going in too low can lose you the property. Data-driven insight makes all the difference here.

With your offer in motion and professionals engaged, it is time to focus on the legal checkpoints: exchange and completion.

Navigating exchange and completion

Exchange of contracts and completion are two distinct legal milestones, and confusing them is a costly mistake. The exchange of contracts is the point at which the sale becomes legally binding for both parties. Completion is when the money transfers, the sale finalises, and you collect the keys.

Before you exchange, confirm the following:

- Your mortgage offer is formally issued in writing

- You have read and understood the draft contract

- All searches (local authority, water, environmental) are back and reviewed

- Buildings insurance is arranged and ready to activate from exchange date

- You have agreed a completion date with all parties in the chain

- Your deposit funds are ready to transfer

| Stage | What happens | Key risk |

|---|---|---|

| Exchange | Contracts signed, deposit paid, date set | Pulling out means losing your deposit |

| Between exchange and completion | Final checks, mortgage funds requested | Chain collapse, last-minute issues |

| Completion | Funds transfer, keys released | Delays can incur daily penalty charges |

Statistic: If you pull out after exchange, you forfeit your deposit, which is typically 10% of the purchase price. On a £300,000 property, that is £30,000 lost. This is why thorough preparation before exchange is non-negotiable.

Using local property data to validate your offer price before exchange gives you one final confidence check. If comparable sales in the area support the price you have agreed, you can proceed knowing you have paid a fair amount.

Finally, let's cover special scenarios that could introduce unexpected requirements or challenges.

Special cases: Property pitfalls and lender requirements

Even when everything appears to be progressing smoothly, certain property features can trigger additional lender requirements or cause a mortgage to be refused entirely. These issues are often only discovered during the survey or solicitor's searches, which is why instructing both promptly is so important.

Common dealbreakers and lender red flags include:

- Short lease: Leases below 80 years are problematic. Below 70 years, many lenders will refuse to lend entirely.

- Non-standard construction: Properties built with concrete panels, timber frames, or steel frames may require specialist lenders and higher deposits.

- Missing rights of way: If the property does not have a legal right of access over a shared driveway or path, this can block a sale.

- Cladding issues: Post-Grenfell, properties with certain cladding types in blocks of flats face significant mortgage restrictions.

- Restrictive covenants: Legal restrictions on how you can use or alter the property, which may affect your plans.

- Japanese knotweed: This invasive plant can affect the structural integrity of a property and many lenders will not lend without a management plan in place.

As the first-time buyer legal checklist makes clear, unusual property features can trigger extra lender requirements or outright refusal to lend. Your solicitor's searches and your surveyor's report are your primary tools for uncovering these issues before they become expensive problems.

Pro Tip: If your surveyor flags anything unusual, ask your solicitor to raise it with the seller immediately. Many issues can be resolved with indemnity insurance or a price reduction, but only if you address them before exchange. Leaving them until the last minute creates pressure and poor decisions.

Having reviewed the checklist, let's share our perspective on what most first-timers get wrong and how to get it right.

What most first-time buyers miss: A perspective on process and pitfalls

Most first-time buyers focus intensely on finding the right property. That is understandable. But the truth is, the property itself is rarely the reason purchases collapse or go badly wrong. The process is.

The single biggest source of delays and failed purchases is poor coordination between the mortgage broker, solicitor, and surveyor. These three professionals need to be working in parallel, not sequentially. Yet buyers often instruct one, wait for news, then instruct the next. That approach adds weeks to a purchase and leaves you exposed to chain collapse and seller impatience.

Communication is everything. Respond to your solicitor's queries the same day. Return calls promptly. Chase your mortgage lender if you have not heard anything for more than a week. The buyers who complete fastest are not the ones with the most money. They are the ones who stay engaged and keep things moving.

There is also an uncomfortable truth about research. Most buyers do not do enough of it upfront. They view a property twice, fall in love with it, and make an offer based on gut feeling. Then they discover during the survey that the roof needs replacing, or the solicitor finds a restrictive covenant that prevents the extension they planned. Doing deeper property checks before you make an offer is not excessive caution. It is basic due diligence.

Over-invest in research before you offer. It costs you nothing but time, and it saves you from the anxiety of discovering problems after you are legally committed.

Next steps: Tools and support for first-time buyers

You now have a clear picture of every stage in the first home buying process. The next step is putting that knowledge into action with the right tools behind you.

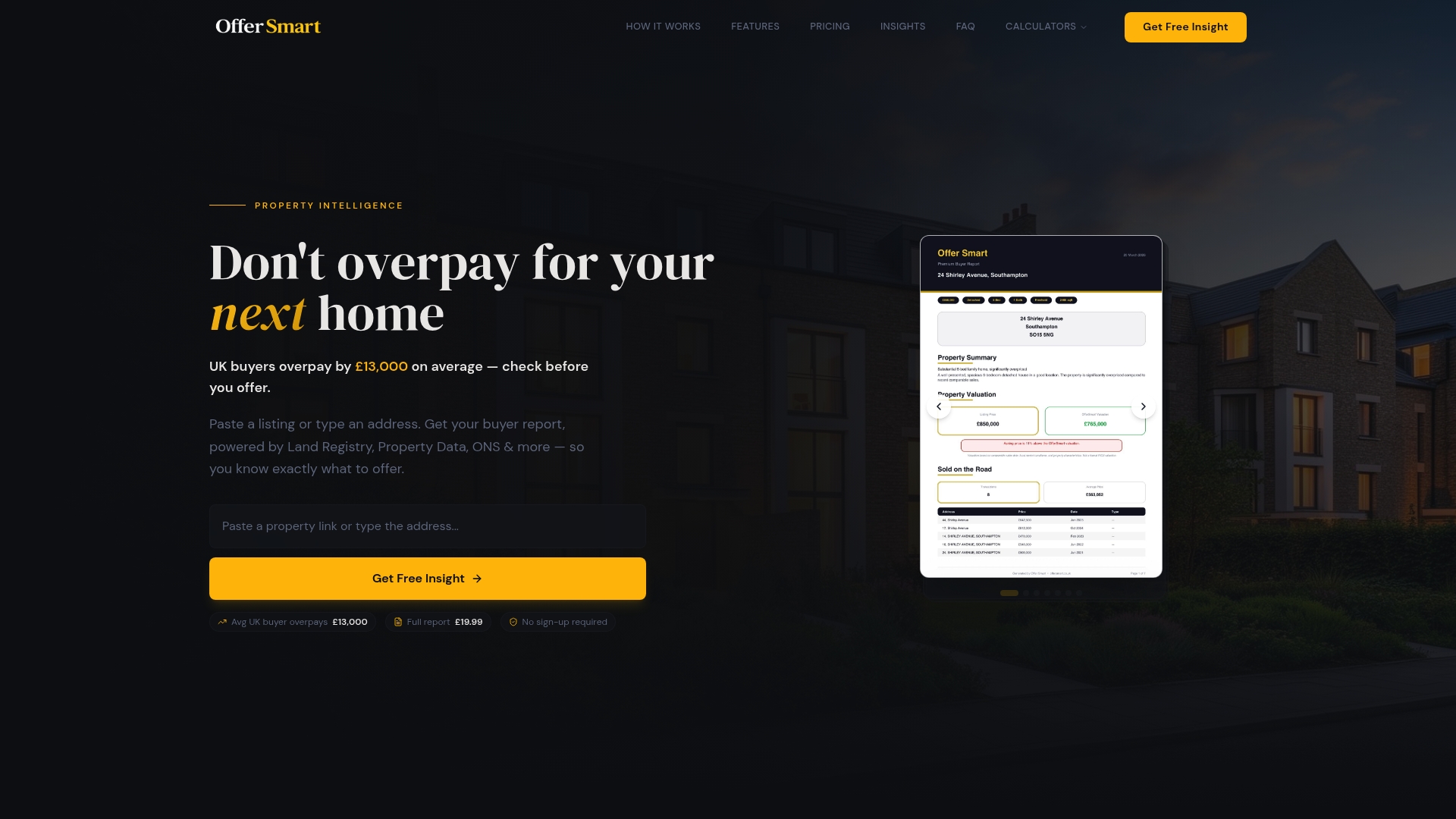

Offer Smart is built specifically for UK buyers who want clarity before they commit. Enter a property address or paste a listing link, and you instantly get a data-driven analysis of what you should realistically offer, based on comparable local sales. You also get flood risk, crime risk, school proximity, and lifestyle data, so you can assess the area as well as the property. Use the built-in UK mortgage calculator to model your monthly payments and understand your true affordability. Explore all the property calculators to plan your budget with precision. Visit the Offer Smart platform today and take the guesswork out of your first purchase.

Frequently asked questions

What is the minimum deposit needed to buy a first home in the UK?

You can buy with as little as a 5% deposit using the Mortgage Guarantee Scheme, available through participating UK lenders from July 2025. A larger deposit will typically secure you a lower mortgage interest rate.

What's the difference between exchange and completion?

Exchange makes the sale legally binding for both buyer and seller, while completion is when funds transfer, the sale finalises, and you collect the keys. The gap between the two is typically one to four weeks.

Is a survey different from the lender's mortgage valuation?

Yes. The lender's valuation only confirms the property is worth the loan amount to the lender. Your independent survey assesses the actual physical condition of the building and protects your interests, not the lender's.

What property issues can stop my mortgage?

Problems such as a short lease, non-standard construction, or missing rights of way can lead lenders to refuse a mortgage or impose additional conditions. Your solicitor and surveyor should identify these issues before exchange.