Buying your first home in the UK is one of the most significant financial decisions you will ever make, yet the process is rarely explained clearly. Estate agents, solicitors, and mortgage brokers each handle their own slice of the transaction, leaving you to piece together a confusing jumble of stages, deadlines, and jargon. Rightmove frames the journey as a structured, step-by-step process, and that is exactly the right approach. This guide breaks your property purchase timeline into five clear stages, giving you a practical checklist at each point so nothing falls through the cracks.

Table of Contents

- Stage 1: Getting financially ready before viewing properties

- Stage 2: Making an offer and instructing a solicitor

- Stage 3: Conveyancing, searches, and pace management

- Stage 4: Exchange, completion, and post-completion essentials

- Stage 5: Variability for new-builds and complex chains

- What most checklist guides miss: managing the advice gap and delay risks

- Take the next step with Offer Smart tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Stage-by-stage process | Break the purchase timeline into clear stages with tasks for each milestone. |

| Legal checkpoints | Exchange and completion are non-negotiable deadlines; plan admin and funds accordingly. |

| Delay management | Allow extra time and actively chase documents to reduce risks of bottlenecks. |

| Variability awareness | New-builds, leaseholds, and complex chains need extra checklist steps and patience. |

| Advice gap | Clarify instructions and check your understanding at every stage to avoid costly mistakes. |

Stage 1: Getting financially ready before viewing properties

Before you book a single viewing, your financial position needs to be solid. This is where many first-time buyers make their first mistake: they fall in love with a property before knowing what they can realistically afford or borrow.

Start with these checklist items:

- Check your credit report with all three major agencies (Experian, Equifax, and TransUnion) and correct any errors at least three months before applying.

- Calculate your maximum budget including deposit, Stamp Duty Land Tax (SDLT), solicitor fees, survey costs, and moving expenses. These additional costs typically add 3 to 5 per cent on top of the purchase price.

- Obtain a Mortgage in Principle (MIP), also called an Agreement in Principle (AIP). This is a written indication from a lender of how much they would lend you. Prioritising AIP/Mortgage in Principle before beginning your search is one of the most important steps you can take.

- Define your search criteria clearly: property type, number of bedrooms, commute distance, freehold versus leasehold, and proximity to schools or transport links.

- Research local market values for your target area so you have a benchmark when offers are needed.

Having your MIP ready signals to estate agents that you are a serious buyer. It can also accelerate the process once an offer is accepted, because your mortgage application is already partway through the lender's system.

Pro Tip: Before viewing any property, complete the buyer checks before making an offer to understand what due diligence you should carry out. If you are also considering buy-to-let, use a rental yield calculator to assess projected returns before you commit.

Stage 2: Making an offer and instructing a solicitor

Once you have found a property you want and your finances are in order, the next stage moves quickly. Speed and clarity matter here because other buyers may be competing for the same home.

Follow this sequence carefully:

- Research comparable sales on the road and in the surrounding area to determine a fair offer price. Understanding local market data removes the guesswork from your negotiation.

- Make your offer in writing via the estate agent, stating your MIP, your position (no chain, first-time buyer), and any conditions.

- Negotiate with confidence. Do not anchor to the asking price alone. For guidance on avoiding overpaying for a house, look at what properties have actually sold for, not what they were listed at.

- Receive written confirmation of your accepted offer before taking any further steps.

- Instruct a solicitor or licensed conveyancer immediately upon acceptance. Delays here are common and costly. According to Money Meister's guide, instructing your solicitor as soon as the offer is accepted is one of the critical momentum-keeping actions in the entire process.

- Provide your solicitor with ID documents, source of funds evidence, and the memorandum of sale sent by the agent.

- Formally submit your full mortgage application to your chosen lender now that you have an agreed price.

Deciding how much to offer is one of the most stressful parts of the process. Many buyers either offer too low and lose the property, or offer too much and overpay. Data-driven research is your best tool here.

"A third of first-time buyers do not fully understand the process. Clarify every stage before you sign anything." A Mortgage Advice Bureau study reported by Today's Conveyancer found this advice gap is real and widespread.

Pro Tip: Do not sign any legal documents until your solicitor has explained what you are committing to. Confirm in writing which stage you are at and what the next action is.

Stage 3: Conveyancing, searches, and pace management

Conveyancing is the legal process of transferring ownership from seller to buyer. It is also the stage where delays are most likely to occur. Checklist discipline here is not optional; it is essential.

Your solicitor will carry out several key tasks during this stage:

- Local authority searches to check planning permissions, road schemes, and environmental factors near the property.

- Water and drainage searches to confirm connections and potential flood or drainage risks.

- Enquiries to the seller's solicitor about boundaries, fixtures and fittings, and any disputes.

- Review of the mortgage offer once your lender formally approves the loan.

- Review of the title deeds to confirm ownership and identify any restrictions or covenants.

Delays in the UK home-moving process have been increasing, driven by capacity constraints within conveyancing firms, stretched mortgage approval teams, and compliance requirements. Building buffer weeks into your timeline is not pessimistic; it is realistic.

For leasehold properties, additional delays are common because of the need to obtain a leasehold management pack from the freeholder or management company. Leasehold bottlenecks are a well-documented cause of extended completion timeframes. Understanding how agents value properties can also help you assess whether the agreed price still stacks up as the legal process unfolds.

Here is a comparison of typical timelines and influencing factors:

| Factor | Freehold purchase | Leasehold purchase |

|---|---|---|

| Typical conveyancing time | 8 to 12 weeks | 10 to 16 weeks |

| Management pack required | No | Yes (can add 4 to 6 weeks) |

| Chain dependency risk | Medium | Medium to high |

| Search turnaround | 2 to 4 weeks | 2 to 4 weeks |

| Common delay triggers | Mortgage approvals, queries | Management company, lease terms |

To keep the process on track, maintain these habits throughout conveyancing:

- Chase your solicitor weekly if you have not had an update.

- Respond to all document requests within 24 to 48 hours.

- Confirm the status of your mortgage application directly with your broker.

- Ask your solicitor to flag any leasehold issues early, particularly around ground rent or service charges.

- Build in at least two extra weeks on top of your expected exchange date.

Stage 4: Exchange, completion, and post-completion essentials

Exchange and completion are the two legal milestones that mark the end of your buying journey. Understanding the difference between them is critical.

Exchange of contracts is the point at which the sale becomes legally binding. Once you exchange, you cannot pull out without losing your deposit (typically 10 per cent of the purchase price). The seller cannot pull out either. Exchange makes the transaction legally binding, and completion follows when the mortgage funds are released and the seller's solicitor confirms receipt.

Completion is the day you get the keys. Your solicitor transfers the purchase funds from the mortgage lender to the seller's solicitor. Once confirmed, the estate agent releases the keys to you.

Here is a week-by-week overview of the final stages after your offer is accepted:

| Week | Key milestone |

|---|---|

| Week 1 | Offer accepted, solicitor instructed, mortgage application submitted |

| Weeks 2 to 3 | Searches ordered, mortgage surveyor visit arranged |

| Weeks 4 to 6 | Search results received, mortgage offer issued |

| Weeks 7 to 9 | Enquiries raised and answered, contract reviewed |

| Week 10 | Exchange of contracts, completion date agreed |

| Week 11 to 12 | Completion day, keys received, post-completion admin |

After completion, work through these final actions in order:

- Collect the keys from the estate agent.

- Confirm the meter readings for gas, electricity, and water.

- Notify your local council for council tax purposes.

- Register your ownership with HM Land Registry (your solicitor will do this, but confirm it).

- Set up buildings insurance from the day of exchange, not completion.

- Update your address with banks, employers, DVLA, and the electoral roll.

Pro Tip: Have your deposit funds, identification, and any signed documents prepared and ready at least three working days before your expected exchange date. Last-minute delays in fund transfers are a common cause of exchange postponements.

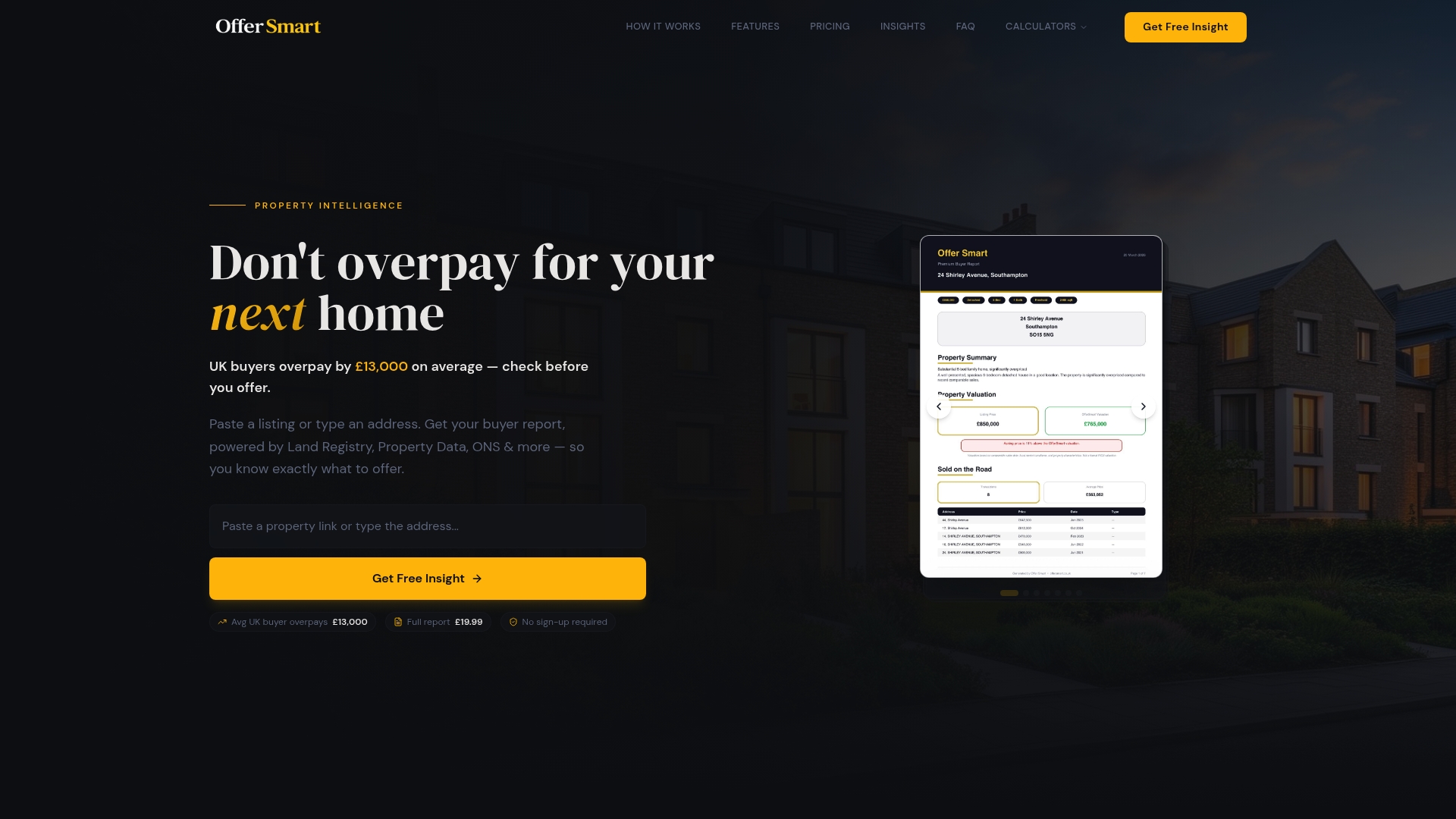

To get ahead before you reach this stage, use Offer Smart to analyse your property address and confirm you have paid a fair price before funds are committed.

Stage 5: Variability for new-builds and complex chains

Not every purchase follows a standard timeline. New-build properties, off-plan purchases, and complex chains each require adjustments to your checklist.

For most buyers, the differences come down to timing, documentation, and communication. Here is what to factor in:

- Completed new-build: The property exists and is ready to move into. Conveyancing is broadly similar to a standard purchase, but new-build warranty documentation (such as NHBC Buildmark) adds an extra review layer.

- Off-plan new-build: You are buying a property that has not yet been built. Off-plan timelines can extend to 12 to 24 months or beyond depending on construction progress. Exchange often happens early, locking in your price but leaving you waiting for completion.

- Chain-free purchase: Typically the fastest route. Without a chain of dependent transactions, you remove one of the most common sources of delay. Aim for chain-free when possible if speed matters.

- Long chain purchases: Every additional link in a chain adds risk. If one buyer or seller delays, it can halt the entire sequence. Your solicitor should map out the chain early and flag any weak links.

- Leasehold purchases: As noted in Stage 3, leasehold adds administrative complexity. Review the lease length carefully. Leases below 80 years can complicate your mortgage and future sale.

Pro Tip: For off-plan new builds, add at least three to six months to your expected timeline and check that your mortgage offer validity period covers the projected completion date. Many mortgage offers expire after six months, requiring a costly reapplication.

What most checklist guides miss: managing the advice gap and delay risks

Most property purchase checklists tell you what to do. Few tell you what to watch out for when things slow down or go wrong. That is the real gap.

A third of first-time buyers do not fully understand the buying process. This is not a criticism; it reflects the fact that the process is fragmented, each professional handles their own part, and no single person takes responsibility for keeping the buyer informed throughout.

The result is that buyers wait passively for updates that do not come, assuming that silence means everything is fine. It rarely does. Increasing delays across the UK market are frequently caused not by complexity alone, but by a lack of proactive chasing at each stage.

Our perspective, shaped by working with buyers across the UK market, is this: your checklist is not just a to-do list. It is a communication framework. Every item on it is an opportunity to confirm progress, identify a bottleneck early, and take action before a delay becomes a collapsed transaction.

Here is what the best-prepared buyers consistently do, which most guides leave out:

- Review your estate agent insights regularly to ensure the agreed price still reflects market conditions as your completion approaches.

- Chase your solicitor every five to seven working days if there is no update, not every few weeks.

- Confirm leasehold documentation status within the first two weeks of instruction, not as an afterthought.

- Ask your mortgage broker specifically when the formal offer will be issued, not just whether it is "in progress."

- Build a minimum two-week buffer into every expected milestone from searches to exchange to completion.

"Checklist discipline turns overwhelm into steady, forward progress, especially when you are proactively chasing rather than passively waiting."

The buyers who complete on time are not necessarily the ones with the simplest transactions. They are the ones who stay engaged, ask direct questions, and treat their checklist as a living document they update weekly.

Take the next step with Offer Smart tools

You now have a clear stage-by-stage framework for your property purchase. The next step is putting the right tools behind each stage so that every decision you make is backed by real data, not guesswork.

Offer Smart gives you a mortgage calculator to map out your affordability before you make an offer, plus a full suite of property calculators covering rental yield, running costs, and long-term value forecasts. Enter any UK address and get an instant analysis of comparable sales, local area data, flood and crime risk, and a realistic offer range. Whether you are at Stage 1 of this checklist or approaching exchange, Offer Smart keeps you informed and in control at every point in the process.

Frequently asked questions

How long does a typical property purchase take for a first-time buyer?

The process commonly takes 8 to 12 weeks from offer acceptance to completion, but leasehold purchases or complex chains can extend this significantly.

What is the difference between exchange and completion?

Exchange is the legally binding commitment point where you cannot withdraw without penalty; completion is when funds are transferred and you collect the keys.

Why are leasehold purchases often delayed?

Leasehold bottlenecks commonly occur because management companies are slow to provide lease packs, and the additional documentation requires more time to review and approve.

How can I avoid delays during conveyancing?

Chase your solicitor, broker, and estate agent proactively every five to seven days, and prepare all documents in advance; increasing conveyancing delays across the market make passive waiting a risk you cannot afford.