Buying a home in the UK is one of the largest financial commitments you will ever make, and the sheer number of variables involved can make the decision feel overwhelming. A clear home buying decision factors list is not a luxury — it is a necessity. Without one, buyers routinely overpay, overlook structural problems, or end up in a neighbourhood that does not suit their lifestyle. This guide walks you through every major factor, ranked by impact, so you can evaluate properties with confidence and make offers grounded in data rather than hope.

Table of Contents

- Essential financial factors when buying a home

- Location and neighbourhood factors to prioritise

- Evaluating home condition and essential features

- Comparison of top home buying decision factors

- Making the best decision based on your priorities

- Rethinking what matters most in a home buying decision

- How Offer Smart helps you make informed home buying decisions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Realistic budgets matter | Set a clear budget including all housing costs to avoid financial surprises after purchase. |

| Location is crucial | Choose a home in a safe area with good schools and amenities to protect value and lifestyle. |

| Prioritise move-in readiness | Focus on structural condition over cosmetic features to reduce unexpected repair costs. |

| Be flexible to succeed | Compromising on non-essential wants increases your chances in a competitive UK market. |

| Use expert tools | Leverage calculators and local data to make informed offers and avoid overpaying. |

Essential financial factors when buying a home

Your home buying decision factors list should begin with money. Not because it is the most exciting topic, but because every other factor becomes irrelevant if you cannot afford the property or sustain the costs of owning it.

Start by understanding your full housing budget. This goes well beyond the mortgage repayment. You need to account for stamp duty, solicitor fees, survey costs, buildings insurance, ground rent (if leasehold), service charges, and ongoing maintenance. A useful rule of thumb: budget at least 1% of the property's value per year for maintenance alone. A £300,000 home could cost you £3,000 annually just to keep in good repair.

Affordability is a genuine barrier for many UK buyers right now. 35% of non-homeowners cite cost of living as the top obstacle to buying, while 23% of existing homeowners point to mortgage rates as their primary challenge. These figures are not abstract. They reflect the reality that millions of buyers are stretching their finances to get onto the property ladder.

When it comes to income allocation, 54% of first-time buyers expect to spend 26 to 35% of their income on housing costs. That is a significant portion of take-home pay, and it leaves little room for error if unexpected expenses arise.

Key financial factors to assess before committing:

- Total purchase costs including stamp duty, legal fees, and survey

- Monthly mortgage repayment relative to your net income

- Buildings and contents insurance premiums

- Service charges and ground rent for flats or leasehold properties

- Estimated utility bills and council tax band for the property

- Emergency repair fund (typically 1 to 3% of property value per year)

Use a mortgage calculator to model different scenarios based on deposit size and interest rate changes. Run the numbers through a stamp duty calculator before you fall in love with any property. And when you are trying to understand whether the asking price reflects actual market value, local property data is your most reliable reference point.

Pro Tip: Get mortgage pre-approval before you begin serious viewings. It tells you exactly what you can borrow, sharpens your negotiating position, and speeds up the process once you find a home you want to offer on.

Now that you understand the financial baseline, let us explore the physical and locational criteria that shape your choice.

Location and neighbourhood factors to prioritise

Experienced buyers will tell you that you can change almost everything about a house. You cannot change where it sits. Location remains the single most influential factor in long-term property value and day-to-day satisfaction.

Location influences home value through a cluster of attributes: neighbourhood safety, school quality, access to amenities, public transport links, and walkability. Each of these contributes independently to desirability and, by extension, to what comparable properties sell for on the same street.

Safety is non-negotiable for most buyers. Check local crime statistics through the Police UK data portal, and pay attention to trends rather than isolated incidents. A neighbourhood with falling crime rates is a fundamentally different investment from one where incidents are rising, even if current numbers look similar on paper.

School catchment areas matter enormously, even if you do not have children. Properties within the catchment zones of Ofsted-rated "outstanding" schools command a consistent price premium. If you are buying as a long-term investment, this factor protects your resale value.

Location factors to evaluate on your home buying checklist:

- Proximity to your workplace and commute time via your typical transport method

- Quality and Ofsted rating of the nearest primary and secondary schools

- Crime risk data at street level, not just postcode level

- Flood risk, especially relevant in many parts of England and Wales

- Access to green space, shops, GP surgeries, and local services

- Planning applications and zoning changes in the surrounding area

- Local employment base and economic trajectory of the area

Visit any area you are seriously considering at different times: a weekday morning, a Friday evening, and a Sunday afternoon. The character of a neighbourhood shifts considerably depending on the time. Understanding how estate agents value properties will also help you decode what is driving asking prices in any given postcode. For broader real estate market insights across different localities, data-driven resources can sharpen your comparative view.

With location clear, let us turn to evaluating the physical condition and features of the home itself.

Evaluating home condition and essential features

A property's condition is one of the most underrated items on any home buying decision factors list. Buyers frequently get distracted by interior styling and underestimate what lies beneath the surface.

Move-in-ready condition is the biggest selling point for most buyers, and structural integrity consistently outweighs cosmetic appeal when it comes to long-term value and buyer satisfaction. A fresh coat of paint and new kitchen worktops are visible and appealing. A failing roof or outdated electrical wiring is invisible until it becomes a very expensive problem.

Before you let yourself become emotionally attached to a property, spend at least 10 minutes testing the basics during your viewing. Run the taps and check water pressure. Turn lights on and off. Open and close windows and doors. Look at the condition of the roof from outside. Check for damp patches, particularly around window frames and in corners. These are not dramatic gestures. They are standard due diligence.

Property condition checks to include in your home buying checklist:

- Roof condition and age (most roofs need replacing every 20 to 30 years)

- Guttering, drainage, and signs of water ingress

- Electrical wiring (does it have a modern consumer unit, or an outdated fuse box?)

- Boiler age and condition, and the last service date

- Damp, mould, or condensation, particularly in bathrooms and kitchens

- Window age and energy rating (double or triple glazed, and the frame condition)

- Signs of subsidence, particularly in older properties or those near trees

Minor kitchen and bathroom updates tend to offer the highest return on investment if you are buying at the lower end of the market. But if a property needs significant structural work, be very realistic about costs before proceeding. Read through what smart property buyers check before making an offer to build your viewing routine into a reliable process.

Pro Tip: Commission a RICS HomeBuyer Survey or a full Building Survey before exchanging contracts. The upfront cost (typically £400 to £1,500 depending on property size and type) is trivial compared to the repair bills you might inherit if you skip it.

Now that you know what physical aspects to assess, let us compare these factors to support your buying strategy.

Comparison of top home buying decision factors

Weighing up different properties becomes far easier when you have a structured framework. The table below compares the core factors influencing home purchase decisions across three key dimensions.

| Factor | Priority level | Changeable after purchase? | Impact on resale value |

|---|---|---|---|

| Financial affordability | Non-negotiable | No | Very high |

| Location and neighbourhood | Non-negotiable | No | Very high |

| School catchment area | High (families) | No | High |

| Structural condition | Non-negotiable | Yes (costly) | High |

| Crime and flood risk | High | No | High |

| Layout and room sizes | High | Partially | Medium to high |

| Kitchen and bathroom quality | Medium | Yes (moderate cost) | Medium |

| Décor and cosmetic finish | Low | Yes (low cost) | Low |

| Garden size and orientation | Medium | No | Medium |

| Energy efficiency rating | Medium to high | Yes (investment needed) | Increasing |

The distinction between non-negotiable and negotiable factors is critical. Buyers who balance needs and wants while staying flexible on non-essential preferences are demonstrably more successful in competitive markets. Holding out for the perfect décor in the right location is the wrong trade-off. Holding firm on flood risk or structural soundness is the right one.

What this means for your buying strategy:

- Fix your non-negotiables before you start viewing, not during

- Be genuinely flexible on cosmetic features and layout tweaks

- Price your wishlist items realistically against budget constraints

- Avoiding overpaying requires knowing market value before you negotiate, not after

With this comparison in mind, we can explore how to apply these insights to your unique buying situation.

Making the best decision based on your priorities

A checklist is only useful if you apply it consistently. Here is a step-by-step approach that puts the key factors in home buying into a workable sequence.

- Define your non-negotiables. Write down the three to five factors you will not compromise on. Location, school catchment, or maximum monthly outgoings are common starting points.

- Set your full budget. Include all purchase costs, not just the deposit and mortgage. Know your ceiling before you start searching.

- Research areas before properties. Spend time in potential neighbourhoods before booking a single viewing. Data on crime, flood risk, and school quality should inform your shortlist.

- Assess each property against your checklist. Use the same criteria every time so you are comparing like with like.

- Commission an independent survey. Never waive this step regardless of how confident you feel about the property.

- Calculate your offer based on comparable sales. Gut feeling is not a negotiation strategy. Market data is.

Buyers open to compromises are significantly more likely to close in low-inventory markets. In much of the UK in 2026, inventory remains tight, so flexibility on your wishlist is genuinely a competitive advantage.

Pro Tip: Use a weighted scoring system for each property you view. Rate each factor from one to five, multiply by its importance weighting, and compare totals. It removes emotion from the short-listing process and surfaces the best overall fit rather than the most recently viewed.

Additional considerations before making an offer:

- Check whether the property is freehold or leasehold, and review lease terms carefully if leasehold

- Confirm council tax band and get an estimate of annual bills

- Understand the local market: are properties selling above or below asking price?

For guidance on structuring your offer, read about calculating property offers and offer pricing strategies based on current market conditions.

Rethinking what matters most in a home buying decision

Here is something most property advice articles will not say directly: the biggest mistakes buyers make are not about properties. They are about priorities.

Buyers consistently overweight cosmetic features. They fall for a well-staged living room, ignore the fact that the boiler is 18 years old, and then spend their first year of ownership managing an unexpected replacement. The staging industry exists precisely because presentation influences emotion, and emotion overrides analysis. Knowing this is happening does not make you immune to it unless you have a written checklist in hand at every viewing.

There is also a persistent tendency to underestimate the role of financial realism in long-term satisfaction. A home that stretches your budget to its absolute limit is not a dream. It is a source of sustained stress. The buyers who report the highest satisfaction with their purchase are generally those who stayed within a comfortable repayment threshold, not those who bought the most expensive property they could technically afford.

Timing matters more than most buyers acknowledge. Getting into the market during a period of high competition and elevated mortgage rates is harder than it looks. But understanding the valuations estate agents work from and matching that against recent comparable sales gives you genuine negotiating power that most buyers simply do not have.

The most data-literate buyers in any given market will always outperform those relying on intuition alone. Not because they are smarter, but because they are asking better questions before they commit.

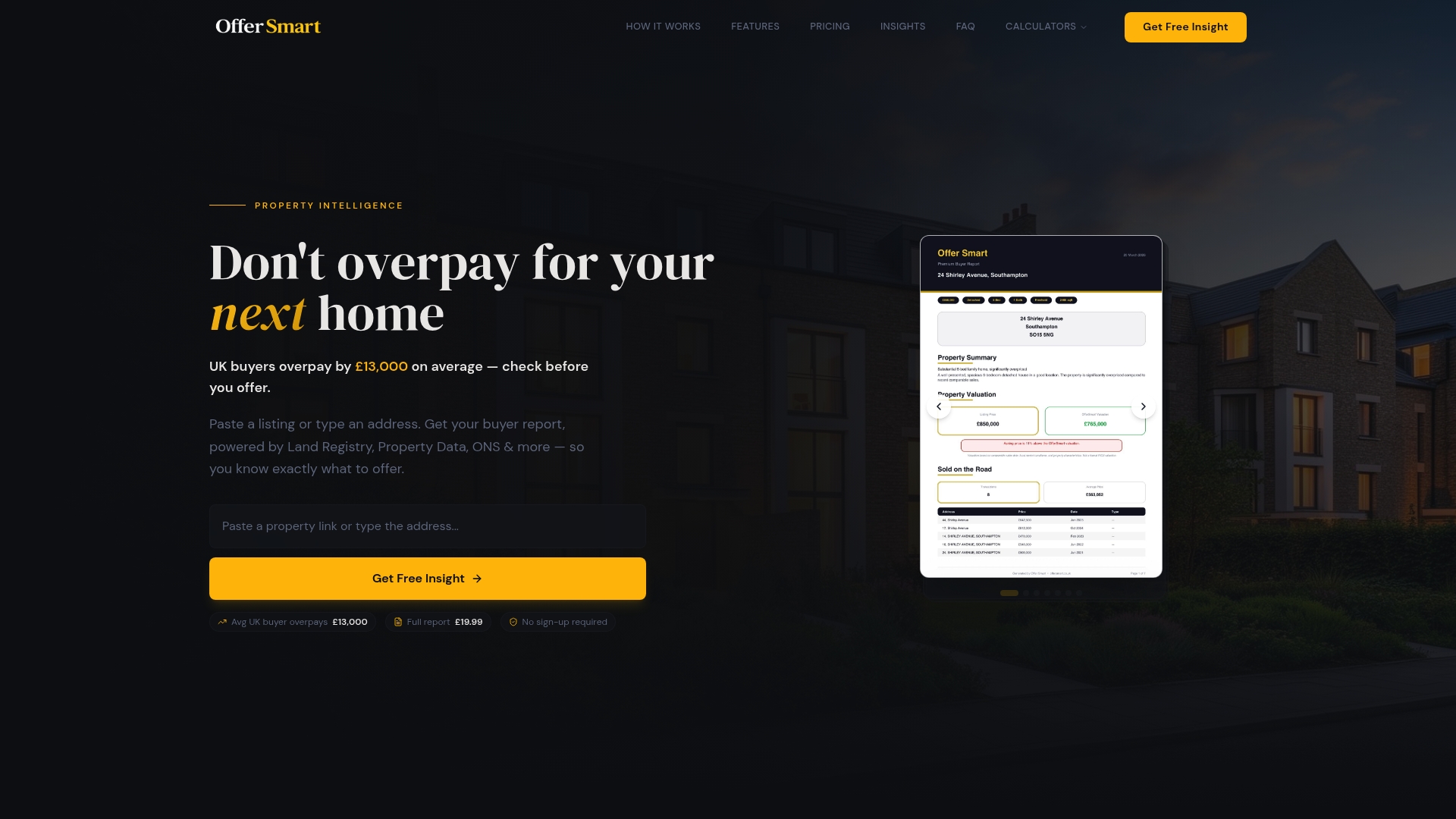

How Offer Smart helps you make informed home buying decisions

Putting together a thorough home buying decision factors list is the right approach. Acting on it with accurate, current data is what separates confident buyers from anxious ones.

Offer Smart gives you the data infrastructure to do exactly that. Enter any UK property address and receive an instant analysis of comparable local sales, market value, crime risk, flood risk, school proximity, and lifestyle factors. Use the mortgage calculator to model your repayments accurately, and explore the full range of home buying calculators covering stamp duty, running costs, and offer price impact. Whether you are a first-time buyer working through your checklist or an investor calculating ROI, Offer Smart replaces guesswork with clarity so you can move forward with confidence.

Frequently asked questions

What are the most important financial factors to consider when buying a home?

Key financial considerations include mortgage repayments, stamp duty, solicitor fees, insurance, and ongoing maintenance costs. 54% of first-time buyers expect to allocate 26 to 35% of their income to housing, so mapping your full cost picture before committing is essential.

How can I evaluate the location when buying a property?

Prioritise neighbourhood safety, school catchment areas, access to local amenities, and flood risk as your baseline criteria. Location shapes home value through all of these attributes simultaneously, which is why it consistently outranks cosmetic features in buyer satisfaction surveys.

Why is move-in-ready condition so important for buyers?

Move-in-ready homes avoid the immediate cost and stress of major repairs, which quickly erode any price advantage from a lower asking price. Structural integrity outweighs cosmetic finish every time when assessing true long-term value.

How can flexibility in must-haves improve my chances of buying a home?

Holding firm only on genuine non-negotiables gives you a far wider pool of viable properties to consider. Buyers who stay flexible on secondary preferences close more successfully in low-inventory markets, which describes much of the UK in 2026.

When should I get mortgage pre-approval during my homebuying process?

Get pre-approved before you attend any serious viewings. Only 22% of first-time buyers secured pre-approval despite having active buying intentions, which means most are negotiating without knowing their actual financial position.