Most first-time buyers assume the mortgage valuation their lender arranges is enough to protect them. It is not. A homebuyer report is distinct from a mortgage valuation and is specifically designed to protect you as the buyer by assessing property condition and risks. The valuation tells your lender whether the property is worth the loan. The homebuyer report tells you whether the property is worth buying. That difference can cost you tens of thousands of pounds if you get it wrong.

Table of Contents

- What is a homebuyer report and what does it cover?

- Difference between homebuyer reports and mortgage valuations

- When should you get a homebuyer report and is it suitable for your property?

- Costs, timing, and what to expect from the homebuyer report process

- How to use your homebuyer report to negotiate and plan repairs

- Why a homebuyer report is your best defence against hidden property risks

- Smart tools to help first-time buyers avoid overpaying

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Homebuyer report purpose | It provides first-time buyers with detailed insights into a property's condition beyond a mortgage valuation. |

| Suitability | Best for conventional UK homes built after 1900 in reasonable condition, not for older or unusual properties. |

| Usage for negotiation | Uses traffic-light urgency ratings to prioritise repairs and negotiate price or contract terms. |

| Typical cost and timing | Starts around £400, with reports delivered within 5-7 working days of inspection. |

| Buyer protection | The report helps avoid costly surprises by highlighting serious defects before contract exchange. |

What is a homebuyer report and what does it cover?

A homebuyer report is a mid-level property inspection carried out by a RICS-registered surveyor (Royal Institution of Chartered Surveyors, the professional body that sets standards for UK property professionals). It uses a visual check of all accessible areas and applies a traffic light rating system to flag issues in order of urgency.

The surveyor does not lift floorboards or open up walls. What they do assess is substantial. A thorough homebuyer report covers:

- Structural condition including walls, floors, ceilings, and roof

- Damp and timber problems such as rising damp, wet rot, or woodworm

- Roofing condition, including visible tiles, chimneys, and guttering

- Windows, doors, and drainage for signs of deterioration or failure

- Insulation and energy performance observations

- A buyer-facing market valuation based on comparable local sales

- An insurance reinstatement cost (the cost to rebuild the property from scratch, which matters for buildings insurance purposes)

- A traffic light urgency rating on every item inspected, ranging from green (satisfactory) to red (urgent attention required)

This final point is often underappreciated. The traffic light system is not just a summary. It tells you exactly which problems need attention now, which can wait, and which are simply informational. For a first-time buyer with no experience of property defects, that structure is genuinely useful.

As part of your wider UK first home buying checklist, commissioning a homebuyer report early in the process prevents you from progressing too far before discovering something costly.

Difference between homebuyer reports and mortgage valuations

Many buyers receive the mortgage valuation report from their lender and assume they are covered. This is one of the most common and expensive misconceptions in UK property buying. Mortgage valuations protect lenders and focus on security for the mortgage, whereas homebuyer reports protect the buyer by assessing condition, defects, and giving actionable advice.

Here is a clear comparison:

| Feature | Mortgage valuation | Homebuyer report |

|---|---|---|

| Who commissions it | Your lender | You, the buyer |

| Who it protects | The lender | You |

| Length and detail | 1-2 pages, brief | 20-30 pages, detailed |

| Condition assessment | Minimal or none | Full visual inspection |

| Traffic light ratings | No | Yes |

| Repair recommendations | No | Yes |

| Buyer-facing valuation | No | Yes |

| Reinstatement cost | No | Yes |

| Useful for negotiation | No | Yes |

The practical implication is significant. A mortgage valuation will not tell you that the roof needs replacing in two years, that there is evidence of damp in the rear bedroom, or that the drainage shows signs of blockage. A homebuyer report will.

You can use that information to avoid overpaying for a house by presenting defects to the seller as grounds for a price reduction. Without the report, you have no basis for negotiation beyond instinct.

When should you get a homebuyer report and is it suitable for your property?

Timing matters. You should commission a homebuyer report after your offer has been accepted but before you exchange contracts. This is the window where you still have the ability to renegotiate or walk away without significant financial penalty.

Suitability is equally important. Homebuyer reports typically suit conventional homes built after 1900 or 1930 in reasonable condition, while older or unusual properties may require a more detailed building survey.

Here is a quick guide to help you decide:

- Good fit for a homebuyer report: Standard brick-built semi-detached or terraced homes, modern flats in conventional buildings, properties that appear structurally sound and have not been heavily altered

- Consider a building survey instead: Pre-1900 properties, thatched or timber-framed homes, properties with significant extensions or conversions, homes in obvious disrepair, listed buildings

- Not suitable for either: Brand-new builds, which are covered by the developer's warranty and a snagging inspection

A building survey goes further than a homebuyer report. It investigates hidden areas more thoroughly and gives detailed advice on remediation. It also costs more, typically starting from £600 to £1,500 or higher depending on the property. But for the right property type, that additional cost is worth every penny.

Pro Tip: If you are unsure which survey suits your property, ask a RICS-registered surveyor for a recommendation before you book. Many offer a free telephone consultation. It takes five minutes and could save you from commissioning the wrong report for a property that needs deeper scrutiny.

Use the home suitability checklist alongside your surveyor's advice to assess whether your chosen property fits standard criteria before booking.

Costs, timing, and what to expect from the homebuyer report process

Understanding the process removes anxiety. Here is what typically happens from start to finish:

- You book the survey directly with a RICS-registered surveyor, either independently or through a referral from your solicitor or estate agent. Always confirm the surveyor is RICS-qualified.

- The surveyor visits the property for approximately two to three hours, conducting a thorough visual inspection of all accessible areas inside and out.

- The report is prepared using a standardised RICS format, producing a document of roughly 20 to 30 pages covering every inspected element with traffic light ratings.

- You receive the report typically within five to seven working days of the inspection.

- You review the findings with your solicitor and, if significant issues are flagged, discuss the implications for your offer or decision to proceed.

On cost, expect to pay from around £400 upwards, with the final figure varying based on property size and value. A flat in a small market town will cost less to survey than a five-bedroom detached house in an expensive postcode. Budget accordingly and treat the cost as an essential part of your purchase, not an optional extra.

Worth knowing: The £400 or so you spend on a homebuyer report is negligible against the cost of discovering structural problems after you have completed. A single undisclosed damp issue can run to £3,000 or more to remediate. A failing roof can cost £5,000 to £15,000. The report pays for itself many times over if it catches even one significant defect.

How to use your homebuyer report to negotiate and plan repairs

Receiving the report is not the end of the process. It is the beginning of a practical conversation about money. The traffic light system is your guide to where to focus your attention.

Here is how to apply the findings:

- Red ratings indicate urgent issues requiring immediate action. These are your strongest negotiation points. Request a price reduction that reflects the estimated repair cost, or ask the seller to fix the problem before exchange.

- Amber ratings highlight defects that need attention in the near future. Factor these into your repair budget and use them as secondary negotiation points if the total cost is significant.

- Green ratings are satisfactory findings that need no action beyond routine maintenance.

- Share specific findings with your solicitor rather than simply saying "the survey found problems." Specific defects, repair costs, and urgency ratings give your solicitor something concrete to work with.

- Get repair estimates before you commit. A builder's quote for any red or amber items gives you hard numbers to present to the seller and supports a realistic price adjustment.

Red or amber flags often justify renegotiating the price or insisting on repairs before exchange, and the traffic light urgency system makes those priorities clear.

Pro Tip: Do not simply present the report to the seller and hope they reduce the price. Frame specific findings as specific costs. "The report identifies urgent roof repairs costed at £4,500. We would like to adjust our offer accordingly" is far more effective than "the survey flagged some issues."

Knowing how much to offer on a house before you even instruct a survey gives you a baseline. Your report then tells you whether that figure needs to come down and by how much.

Why a homebuyer report is your best defence against hidden property risks

Here is the perspective you will not often hear: most first-time buyers treat the homebuyer report as a box to tick, something to arrange because a solicitor mentioned it. That misses the point entirely.

The homebuyer report functions as decision-support for buyers, not just paperwork, helping avoid costly post-purchase issues and providing genuine peace of mind. Think about what that actually means. You are about to commit to the largest financial transaction of your life, likely based on two or three viewings of a property you inspected for under an hour combined. The homebuyer report is the only document in the entire purchase process written entirely for your protection.

Conventional wisdom in UK property buying pushes buyers toward speed. Get your offer in. Do not lose the property. Move fast. That pressure often leads buyers to skip detailed surveys or choose the cheapest option to avoid delays. It is a false economy. The buyers who skip proper surveys and later discover rising damp, failing lintels, or drainage issues are not unlucky. They were under-informed.

What makes the homebuyer report particularly powerful is the combination of condition data and negotiation structure. You do not just find out what is wrong. You find out how urgent it is, and that urgency becomes your negotiating language. A red-rated roof is not just "a problem." It is a quantifiable liability you can price and present.

The alternative, buying on instinct and a brief mortgage valuation, leaves you carrying all the risk. A surveyor carries professional indemnity insurance. If they miss something they should have caught, you have recourse. That protection disappears the moment you choose not to commission the report at all.

For anyone following a first home buying checklist, the homebuyer report belongs near the top. Not as a formality, but as an active tool for buying with confidence.

Smart tools to help first-time buyers avoid overpaying

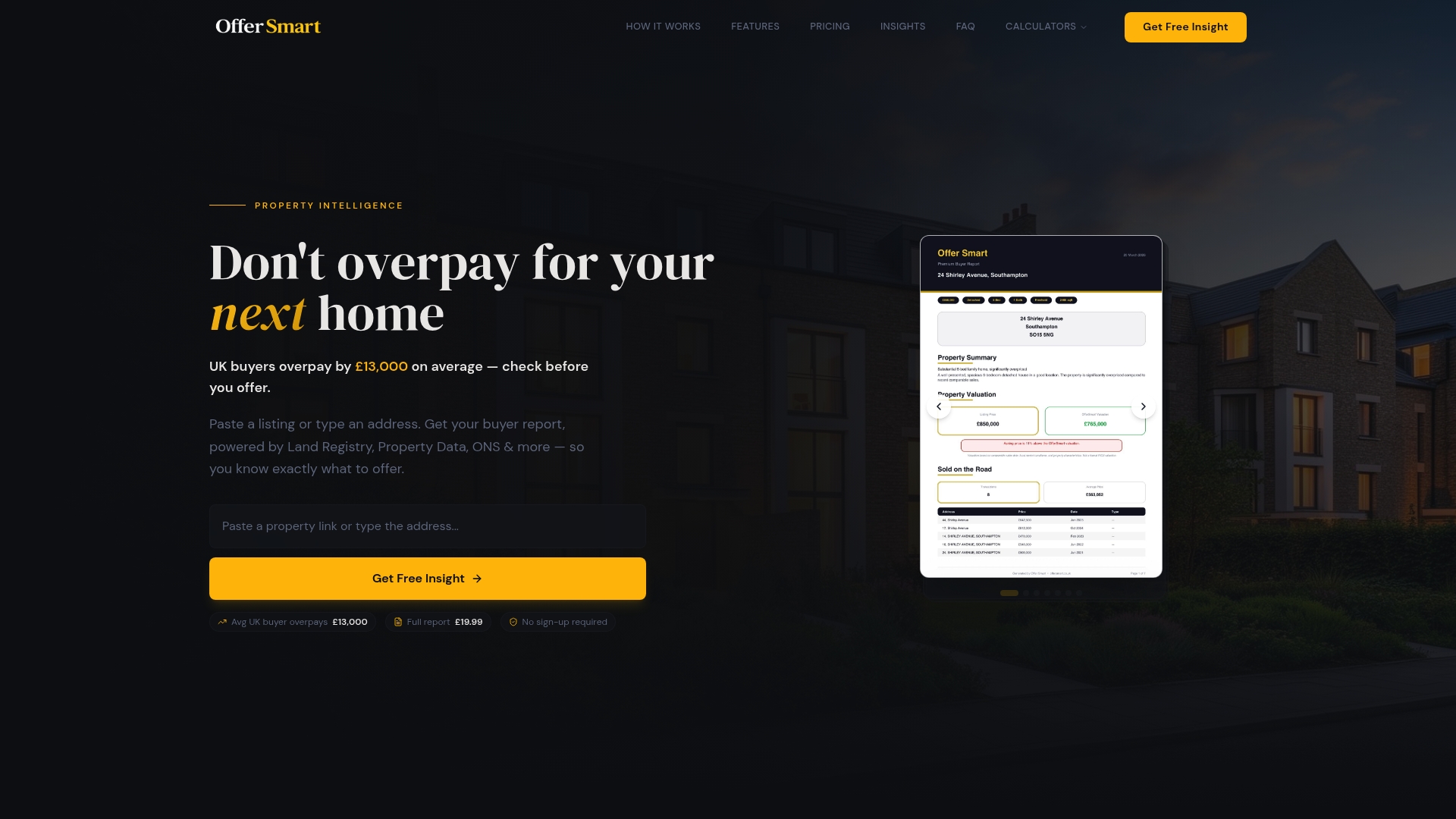

A homebuyer report tells you what condition a property is in. But before you even get to that stage, you need to know whether the asking price is realistic. That is where Offer Smart comes in.

Enter any UK property address or paste a listing link into Offer Smart and you instantly see recent comparable sales on the same road, flood risk, crime data, nearby schools, and a five-year value forecast. A built-in mortgage calculator helps you understand your borrowing limits before you make an offer, and our suite of property value calculators gives you a transparent picture of what the home is genuinely worth in today's market. Pair those insights with your homebuyer report findings and you are negotiating from a position of real knowledge, not guesswork.

Frequently asked questions

How soon after a survey does the homebuyer report arrive?

You can usually expect the homebuyer report within five to seven working days after the surveyor visits the property. Delivery within this window and a standardised 20 to 30 page format is typical for homebuyer reports in the UK.

Is a homebuyer report the same as a mortgage valuation?

No. A homebuyer report focuses on the property's condition for your protection as the buyer, while a mortgage valuation is arranged for the lender's security and does not assess defects. Mortgage valuations protect lenders; homebuyer reports protect you.

Can a homebuyer report help me negotiate the house price?

Yes. Serious defects flagged by the report can support price renegotiation or repair demands before contracts are exchanged, giving you concrete grounds to adjust your offer.

Are homebuyer reports suitable for older or unusual properties?

They are generally suitable for conventional properties built after 1900. Older or unusual properties such as listed buildings, timber-framed homes, or heavily altered houses typically require a more comprehensive building survey.

What if the homebuyer report reveals major problems?

You have three options: budget for the repairs and adjust your offer, negotiate with the seller to carry out the work before exchange, or walk away entirely. The report helps you spot serious defects early, giving you control before you are legally committed.