Putting in an offer on a house feels like it should be simple. You find a property you love, agree on a number, and the estate agent takes care of the rest. That is a common assumption, and it is also why so many first-time buyers find themselves underprepared. Understanding what is making an offer process really involves goes well beyond a phone call to an agent. It requires research, a clear financial picture, smart negotiation, and a firm grasp of the legal realities specific to England and Wales. This guide walks you through every stage, from preparation to acceptance and beyond.

Table of Contents

- Key takeaways

- What is the making an offer process?

- Laying the groundwork before you bid

- How to structure and present your offer

- Navigating negotiations and counteroffers

- What happens after your offer is accepted

- My honest perspective as someone deep in UK property

- Make your offer with confidence using Offersmart

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Prepare before you offer | Secure a Mortgage in Principle before approaching any seller to strengthen your position. |

| Research drives your opening bid | Use comparable sales data to justify your offer rather than guessing from the asking price. |

| Offers are not legally binding | Neither party is legally committed until contracts are exchanged, so stay strategic throughout. |

| Written confirmation matters | Always follow a verbal offer with written confirmation to protect yourself and avoid disputes. |

| Post-acceptance steps are critical | Instruct a conveyancer quickly after acceptance to keep the transaction moving forward. |

What is the making an offer process?

The making an offer process is the sequence of steps you take from deciding you want a property through to having your offer formally accepted and the post-acceptance legal work underway. It covers financial preparation, market research, structuring your bid, communicating with the estate agent, negotiating, and understanding what happens after a seller says yes.

Many first-time buyers treat this as a single moment rather than a multi-stage process. The reality is that each stage builds on the one before it. Skipping the preparation phase, for example, leaves you without the data to justify your offer or the mortgage evidence to convince a seller you are a credible buyer. Getting the process right puts you in a significantly stronger position at every step.

Laying the groundwork before you bid

Getting your mortgage in principle

Before you contact any estate agent, secure a Mortgage Agreement in Principle, also known as a Mortgage in Principle or AIP. This is a conditional statement from a lender confirming how much they would be willing to lend you. An AIP typically takes 10 minutes online and is valid for 30 to 90 days, with some lenders extending this to six months.

Having an AIP does two things. It tells you your realistic budget before you fall in love with a property that is out of reach. It also signals to sellers and agents that you are a serious buyer with finance in place, which carries real weight when multiple offers are on the table.

Beyond your deposit and mortgage, factor in the full cost of buying:

- Stamp Duty Land Tax (applicable above certain thresholds for first-time buyers)

- Solicitor and conveyancer fees, typically £1,000 to £2,500

- Survey costs, ranging from a basic condition report to a full structural survey

- Mortgage arrangement and valuation fees

- Removal costs and any immediate home improvement expenses

Pro Tip: Use Offersmart's mortgage calculator before you start viewing properties. Knowing your exact affordability ceiling means you can set a firm maximum offer and stick to it under pressure.

Researching comparable sales

Your opening offer should not be based on the asking price alone. Sellers and their agents set asking prices, and those prices do not always reflect what a property is realistically worth in the current market. Use HM Land Registry data and property portals to find recent sold prices on the same road and in the immediate area. Look for properties with similar square footage, bedroom count, and condition sold within the last three to six months.

This data gives you a factual basis for your offer. When you can point to three comparable sales at a certain price level, your lower bid carries weight instead of just feeling like a lowball attempt. Understanding offer price in UK buying before you bid is one of the most useful things you can do as a first-time buyer.

How to structure and present your offer

Setting your opening bid

Research generally suggests that starting 5 to 10% below asking price is a reasonable opening position in most markets, though this varies considerably with supply and demand in a given area. In a slow market with a property that has been listed for several months, you may have room to go lower. In a competitive market where properties are selling within days, bidding close to or at asking price may be necessary from the outset.

The goal of your opening bid is to leave room to negotiate upward while not insulting the seller into dismissing you entirely. Ground your bid in the comparable sales data you have gathered.

Presenting your buyer profile

Being chain-free, having a mortgage in principle, and offering flexibility on completion timing can matter as much as price to many sellers. A seller who needs to move quickly for a job relocation will often favour a buyer who can complete in six weeks over one offering slightly more money but tied up in a complicated chain.

When making your offer, tell the agent these facts clearly:

- Confirm you have your AIP in place

- State whether you are chain-free (no property to sell before you can proceed)

- Indicate your preferred timeline for exchange and completion

- Mention your solicitor is already instructed or ready to be instructed promptly

Confirming your offer in writing

Make your offer verbally to the estate agent, then follow up immediately with a written confirmation by email. This creates a clear record of the figure agreed, any conditions attached, and the date of the offer. Verbal agreements in property are easily misremembered or disputed. Email records protect you and keep the process transparent.

Pro Tip: When submitting a lower offer, briefly explain the reasoning in your email. Reference the comparable sales you found and note any work the property needs. A respectful, evidence-based justification lands far better than a bare number and increases the chance the seller will respond positively rather than dismissing the offer outright.

Navigating negotiations and counteroffers

Receiving a counteroffer is entirely normal and should not rattle you. It simply means the seller is willing to negotiate rather than rejecting you. Here is how to approach the back-and-forth:

- Pause before responding. You do not need to reply immediately. Taking 24 hours to consider a counteroffer signals that you are thoughtful rather than desperate.

- Know your ceiling before you start. Set your maximum budget before the negotiation begins and commit to it. Emotional attachment to a property is the fastest route to overpaying.

- Ask the agent for context. Estate agents can share information about seller circumstances such as timescales, motivations, and any pressure to sell. This is legitimate and useful intelligence for shaping your approach.

- Use survey findings as leverage. If negotiations stall and you proceed to survey stage, a survey identifying structural issues or required maintenance gives you documented grounds to renegotiate the price. Many buyers successfully reduce the agreed price at this stage rather than pulling out.

- Make a best and final offer strategically. If you have assessed the property's value carefully and are at your limit, making a clear best and final offer can close negotiations. Only use this tactic when you genuinely mean it.

- Document everything in writing. Every agreed revision to price or conditions should be confirmed by email through the agent, creating a clear audit trail.

One crucial legal point: estate agents are legally required to present all offers to the seller, no matter how low. You never need to worry that a reasonable offer is being filtered out before the seller hears it. This also means low offers are not inherently a waste of time. If the property has been on the market for a long time, the seller has already heard the full range of market feedback.

Stay professional throughout. A calm, factual tone keeps dialogue open. Sellers often prefer buyers they feel comfortable with when price differences are marginal.

What happens after your offer is accepted

Offer acceptance feels like the finish line. In reality, it is the start of a new phase. An accepted offer in the UK creates no legally binding obligation until contracts are formally exchanged. Either party can withdraw before that point, though doing so may mean losing non-refundable costs.

Here is what you should do and expect from this point:

- Instruct your solicitor or conveyancer immediately. Delays here cost time and can give sellers a reason to consider other buyers. Instructing a conveyancer promptly after acceptance is one of the clearest signals you can send that you are serious about completing.

- Arrange your property survey. Choose the survey type appropriate to the property. Older homes warrant a full structural survey. New builds are typically covered by a snagging inspection.

- Progress your mortgage application. Your AIP now becomes a full mortgage application. Your lender will conduct their own valuation of the property at this stage.

- Stay on top of communication. Ask your solicitor for weekly updates. Chase if things go quiet. The conveyancing process involves multiple parties and can stall without active management.

- Understand the risk of gazumping. A seller can accept a higher offer from another buyer before contracts are exchanged. You can reduce this risk by requesting the property is taken off the market after your offer is accepted, though sellers are not obligated to agree.

The period between acceptance and exchange is typically 8 to 12 weeks. Read through the homebuying process timeline so you know exactly what milestones to expect and when.

My honest perspective as someone deep in UK property

I have seen first-time buyers lose good properties not because someone outbid them, but because they arrived unprepared. No AIP, no research, no clear sense of their maximum. When a counteroffer came, they panicked and either overpaid or stalled long enough for a more organised buyer to step in.

The offer process rewrites in your favour the moment you treat it as a research exercise rather than a gut-feel moment. I have seen buyers successfully negotiate £15,000 off an asking price simply by presenting three comparable sales from the same street. That is the kind of leverage that comes from preparation, not luck.

The legal non-binding nature of UK offers cuts both ways. Yes, a seller can walk away before exchange. But so can you, without penalty, if something in the survey or conveyancing raises a concern. Too many buyers become emotionally committed far too early and find themselves unable to walk away from a bad deal. Stay clear-headed. The right property will not slip away because you took two days to think through a counteroffer.

Finally, do not underestimate how much your buyer profile matters. Financial readiness and reliability are genuinely persuasive to most sellers. Lead with them every time.

— Rhys

Make your offer with confidence using Offersmart

You now understand the steps. The next question is: how do you know what to actually offer?

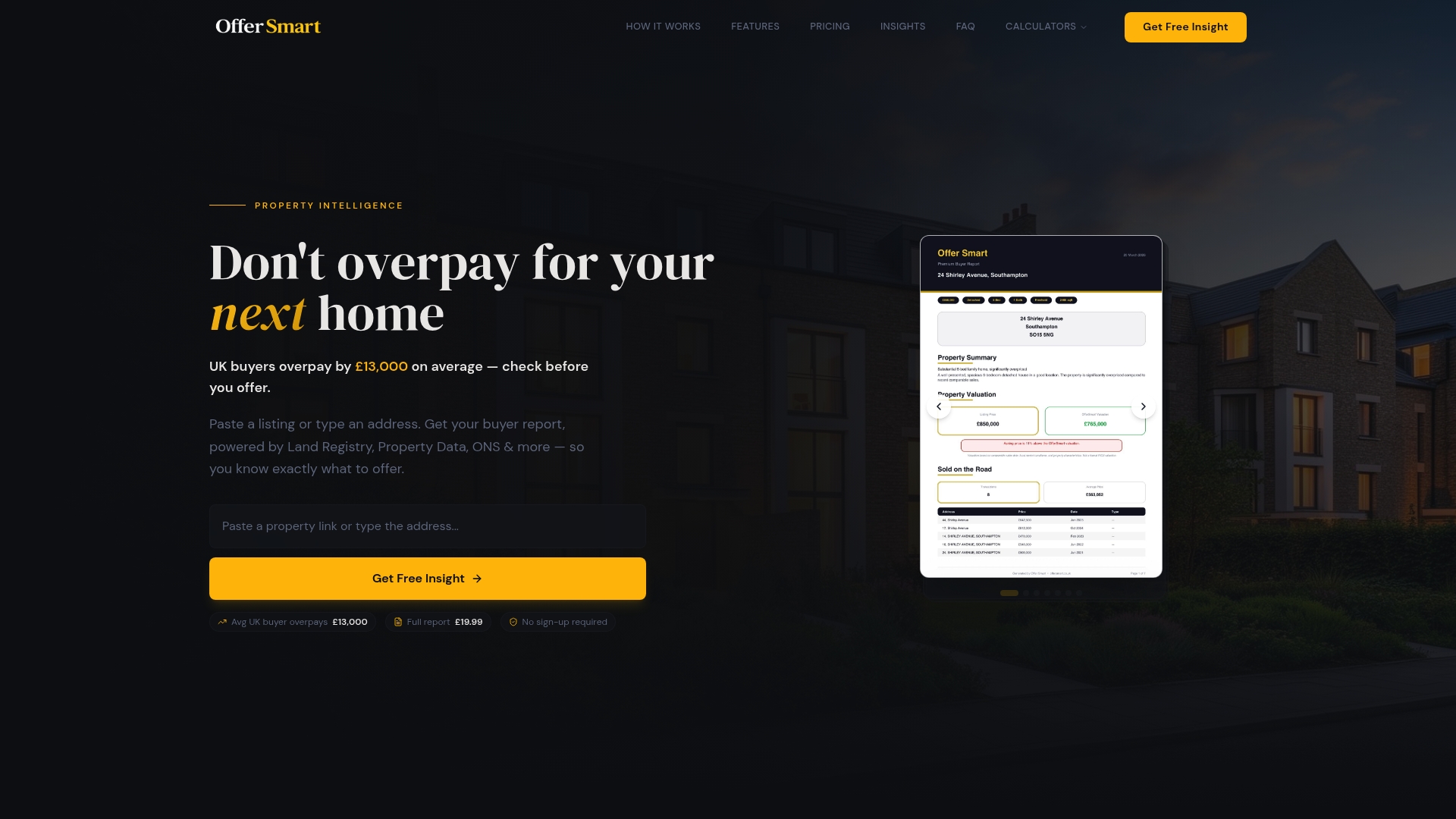

Offersmart removes the guesswork from that decision entirely. Enter a property address or paste a listing link, and Offersmart analyses recent comparable sales on the same road, giving you a clear, data-backed figure to work from. It also covers flood risk, crime data, local schools, and a 5-year value forecast so you understand the full picture before committing. Use the mortgage calculator to confirm your affordability and estimated running costs, then go into your negotiation knowing exactly what the property is worth and what you can comfortably pay. Visit Offersmart to get your buyer report before you make your next offer.

FAQ

What is the making an offer process in the UK?

The making an offer process involves researching comparable sales, securing a Mortgage in Principle, submitting a bid through the estate agent, negotiating, and following up in writing. It ends when an offer is accepted, though legal commitment only occurs at exchange of contracts.

Is a verbal offer on a house legally binding?

No. In England and Wales, neither a verbal nor a written offer is legally binding until contracts are formally exchanged. Both parties can withdraw without legal penalty before that point, though non-refundable costs may be lost.

How much below asking price should I offer?

A common starting point is 5 to 10% below asking price, adjusted for market conditions, time on market, and comparable local sales. In competitive markets, offering at or close to asking price may be necessary.

Do estate agents have to pass on all offers?

Yes. Agents are legally required to present all offers to the seller, regardless of the amount. You can make a low offer with confidence that it will reach the seller.

What should I do immediately after my offer is accepted?

Instruct your solicitor or conveyancer without delay, arrange your property survey, and progress your full mortgage application. These steps protect your position and keep the transaction moving before exchange of contracts.