A first-time buyer is defined as a person who has never owned a freehold or leasehold interest in a residential property anywhere in the world. This legal definition, set by HMRC, determines whether you qualify for Stamp Duty Land Tax (SDLT) relief and a range of government-backed mortgage schemes. Getting this definition right before you purchase is not a formality. It is the difference between saving thousands of pounds and missing out entirely. The UK property market offers genuine financial advantages to qualifying buyers, but only if you understand exactly what the status means and whether you truly hold it.

What is a first time buyer under UK law?

The official term used by HMRC and the UK government is "first-time buyer," and the legal definition is stricter than most people expect. According to HMRC, previous ownership anywhere in the world disqualifies you from first-time buyer status for SDLT relief purposes. This includes property owned abroad, a small share in a jointly owned home, or a property you were added to as a named party on the deeds.

The practical implications are significant. First-time buyer SDLT relief means you pay 0% on the first £300,000 of a property's purchase price, and 5% on the portion between £300,000 and £500,000. Properties priced above £500,000 attract standard SDLT rates regardless of your buyer status. On a £350,000 purchase, that relief saves you £5,000 compared to a standard buyer. That is not a marginal benefit.

Here is what disqualifies you from first-time buyer status for SDLT purposes:

- Owning or having owned any residential property in the UK or overseas, regardless of how long you held it

- Inheriting a property, even if you never lived in it or sold it quickly

- Being added to the deeds of another person's property, such as a parent's home

- Holding a share in a property through a company or trust structure

- Owning a commercial property with a residential element attached

Pro Tip: If you were ever added to a parent's mortgage or deeds to help them remortgage, you may have unknowingly acquired a legal interest in that property. Check with a solicitor before assuming you qualify as a first-time buyer.

For joint purchases, the rule is equally firm. All purchasers in a joint transaction must be first-time buyers to qualify for SDLT relief. If one buyer has previously owned property, the relief is lost for the entire transaction. This catches many couples off guard, particularly where one partner owned a property before the relationship.

How do mortgage schemes support first-time buyers?

The 2025 Mortgage Guarantee Scheme is the primary government mechanism for improving mortgage access for first-time buyers. The scheme enables eligible buyers to secure mortgages with deposits as low as 5%, by providing government-backed guarantees to lenders offering 91% to 95% loan-to-value mortgages. Without this guarantee, most lenders would not offer high loan-to-value products at competitive rates, as the risk exposure is too great.

The scheme works by sharing the lender's risk with the government. This means a lender can offer you a 95% mortgage knowing that if you default, the government covers a portion of the loss. The result is improved mortgage affordability and availability for buyers who have saved a 5% deposit but cannot yet reach the 10% or 15% thresholds that unlock standard mortgage products.

To understand how lender eligibility criteria work in practice, consider these steps:

- Confirm your deposit amount. The scheme requires a minimum 5% deposit of the property's purchase price.

- Check the property type. The scheme applies to residential properties only. New-build homes may have separate eligibility rules depending on the lender.

- Verify your income and affordability. Lenders still apply their own affordability assessments. The scheme does not override standard income multiples or credit checks.

- Understand lender variations. Not every lender participates in the scheme. Barclays, Halifax, Lloyds, NatWest, and Santander have all participated in previous iterations, but you should confirm current participation directly.

- Separate scheme eligibility from SDLT eligibility. You can qualify for the Mortgage Guarantee Scheme without qualifying for SDLT relief, and vice versa. These are distinct criteria.

Pro Tip: Being eligible for the Mortgage Guarantee Scheme does not automatically mean you are a first-time buyer for tax purposes. Always verify your SDLT status separately with a conveyancer before exchange.

How is "first-time buyer" defined in statistics and market data?

The term "first-time buyer" appears frequently in housing market reports, ONS data, and lender publications, but the definition used in those contexts often differs from the legal one. The English Housing Survey defines a recent first-time buyer as someone who purchased their first home within the last three years and had no prior ownership. This three-year lookback is a statistical convenience, not a legal threshold.

Mortgage market data labelled as "first-time buyer" can vary further, because lenders apply their own reporting criteria. Some lenders classify joint borrowers differently, and remortgaging scenarios can affect how a buyer is categorised in datasets. This means the headline figures you read in the press about first-time buyer numbers may not reflect the strict legal definition used by HMRC.

| Context | Definition used | Key distinction |

|---|---|---|

| HMRC / SDLT relief | Never owned property anywhere, ever | Strictest definition; global scope |

| Mortgage Guarantee Scheme | Eligible buyer with 5% deposit; lender criteria apply | Scheme-specific; not tied to SDLT status |

| English Housing Survey | First purchase within the last three years | Statistical lookback; not a legal threshold |

| Lender mortgage data | Varies by lender; joint borrowers may be classified differently | Inconsistent; not a reliable eligibility guide |

Reading a news headline that says "first-time buyer numbers rose last year" does not tell you which definition was applied. For your own eligibility, only the HMRC definition matters when it comes to tax relief.

What practical steps should first-time buyers take before purchasing?

Understanding your eligibility is the starting point, but translating that into a successful purchase requires preparation across several areas. The first-time buyer benefits available in the UK are genuinely valuable, but they require honest, accurate declarations to HMRC. Providing incorrect information about your buyer status is a serious legal matter, not an administrative oversight.

Before you make an offer, work through these key considerations:

- Audit your ownership history honestly. Think back through any property-related transactions, including overseas property, inherited assets, or shared ownership arrangements. If you are uncertain, consult a solicitor before proceeding.

- Check your joint buyer's status. If you are purchasing with a partner, friend, or family member, confirm that they also have no prior ownership. One disqualified buyer removes the SDLT relief for both of you.

- Plan your deposit carefully. The Mortgage Guarantee Scheme opens the door at 5%, but a larger deposit reduces your monthly repayments and may unlock better interest rates. Use a mortgage calculator to model different scenarios before committing.

- Understand the SDLT thresholds. Relief applies only to properties up to £500,000. If you are considering a property above this threshold, factor in the full standard SDLT cost from the outset.

- Seek professional advice early. A conveyancer or solicitor who specialises in residential property can confirm your eligibility before you are committed to a purchase. This is not an area to rely on general internet research alone.

Pro Tip: If you inherited a property and sold it immediately, you may still have held a legal interest, even briefly. HMRC's position is that ownership duration is irrelevant. Get written confirmation from a solicitor if this applies to you.

For a practical walkthrough of the full purchase process, the homebuying process timeline guide covers each stage from mortgage agreement in principle through to completion. And if you want to avoid the most common errors, the first home buying checklist is worth reviewing before you make any formal commitments.

Key takeaways

First-time buyer status in the UK is a strict legal definition set by HMRC, and misunderstanding it costs buyers thousands of pounds in lost SDLT relief.

| Point | Details |

|---|---|

| Legal definition is global | Any prior property ownership anywhere in the world disqualifies you from SDLT relief. |

| Joint buyers must both qualify | If one buyer previously owned property, SDLT relief is lost for the entire purchase. |

| SDLT relief has a price cap | Relief applies only to properties up to £500,000; above this, standard rates apply. |

| Mortgage scheme eligibility differs | The 2025 Mortgage Guarantee Scheme has its own criteria, separate from SDLT status. |

| Statistical definitions vary | Media and survey data use looser definitions; only HMRC's definition governs tax relief. |

Why the definition matters more than most buyers realise

I have seen buyers lose thousands of pounds in SDLT relief because they assumed their situation was straightforward. The most common mistake is not the obvious one. It is not someone who owned a flat for five years and forgot. It is someone who was added to a parent's mortgage at 22 to help them refinance, held that legal interest for six months, and then genuinely forgot it ever happened. A decade later, they are buying their first home and declare themselves a first-time buyer in good faith. HMRC does not accept good faith as a defence.

The second pattern I see regularly is couples where one partner owned a property in another country before moving to the UK. They assume the UK definition applies only to UK property. It does not. HMRC's scope is global, and ownership anywhere disqualifies you from relief. This is not widely understood, and the financial consequences of getting it wrong are not trivial.

What I would tell any buyer is this: do not self-diagnose your eligibility based on a general understanding of the rules. The definition is precise, the stakes are real, and a 30-minute conversation with a conveyancer before you make an offer costs far less than a wrongly claimed relief that HMRC later claws back. The buyers who navigate this well are the ones who treat the definition as a legal question, not a common-sense one.

— Rhys

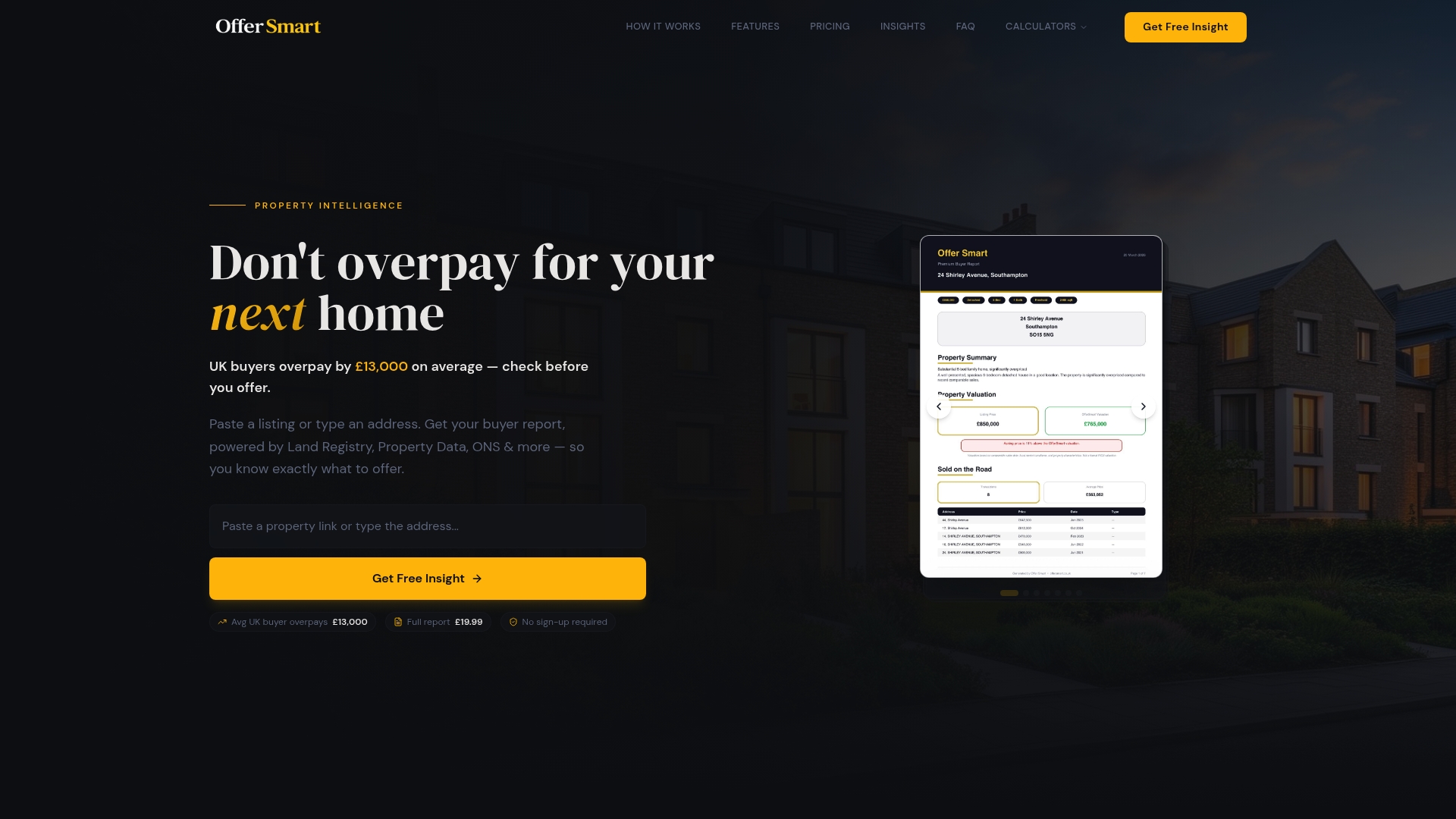

Plan your purchase with confidence using Offersmart

Understanding your first-time buyer status is the foundation. Building the full financial picture around it is the next step.

Offersmart gives you the tools to do exactly that. The mortgage calculator lets you model repayments across different deposit sizes and interest rates, so you can see clearly what you can afford before you make an offer. The stamp duty calculator shows you precisely how much SDLT you will pay based on the purchase price and your buyer status. Beyond the numbers, Offersmart analyses comparable local sales, flood risk, crime data, and school proximity so you are not just calculating costs. You are making a fully informed decision. No guesswork. No surprises.

FAQ

What does first time buyer mean in the UK?

A first-time buyer is someone who has never owned a freehold or leasehold interest in a residential property anywhere in the world. This definition is set by HMRC and determines eligibility for Stamp Duty Land Tax relief and certain mortgage schemes.

Who is considered a first time buyer for stamp duty purposes?

HMRC considers you a first-time buyer for SDLT relief only if you have never previously owned property, including inherited property, overseas property, or a share in a jointly owned home. For joint purchases, all buyers must meet this criterion.

Can I be a first time buyer if I inherited a property?

No. Inherited property counts as ownership under HMRC's rules, regardless of how long you held it or whether you ever lived in it. You would not qualify for first-time buyer SDLT relief.

How does the 2025 Mortgage Guarantee Scheme help first time buyers?

The 2025 Mortgage Guarantee Scheme allows eligible buyers to purchase with a 5% deposit by providing government-backed guarantees to lenders on 91% to 95% loan-to-value mortgages. Eligibility for this scheme is assessed separately from SDLT first-time buyer status.

Does the English Housing Survey use the same definition as HMRC?

No. The English Housing Survey defines a recent first-time buyer as someone who purchased their first home within the last three years. This is a statistical definition used for demographic research and does not reflect the legal threshold HMRC applies for tax relief purposes.