Getting an offer accepted on a property feels like crossing the finish line. It is not. Understanding how property offer acceptance works is the first thing every UK buyer needs to get right, because the acceptance of an offer is not legally binding in England and Wales. It is the start of a process, not the end of one. From solicitors and surveys to gazumping risks and negotiation tactics, a great deal happens between a seller saying yes and you getting the keys. This guide walks you through every stage, clearly and without jargon.

Table of Contents

- Key takeaways

- How the property offer process works

- Steps after offer acceptance

- How sellers assess and compare offers

- Negotiation nuances and handling counteroffers

- Avoiding pitfalls and securing the sale

- My take on what buyers consistently get wrong

- Know your numbers before you offer

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Acceptance is not binding | In England and Wales, an accepted offer carries no legal obligation until contracts are exchanged. |

| Seller responses vary | Sellers may accept, reject, or counter your offer, often requiring several rounds of negotiation. |

| Post-acceptance steps matter | Instructing solicitors, completing surveys, and finalising your mortgage all happen after acceptance. |

| Buyer strength counts | A mortgage in principle and chain-free status can make a lower offer more attractive than a higher, uncertain one. |

| Gazumping is a real risk | Moving quickly on legal and mortgage steps after acceptance significantly reduces your exposure. |

How the property offer process works

When you make an offer on a property in the UK, you submit it verbally or in writing through the estate agent. The agent is legally required to pass every offer to the seller. From there, the seller weighs up their options.

Seller responses typically fall into one of three categories: outright acceptance, rejection, or a counteroffer that opens a negotiation. Most transactions involve at least one round of back-and-forth before both parties settle on a figure. Do not be surprised if your first offer is met with a counter rather than a yes.

What many buyers do not realise is that sellers are not evaluating price alone. Your position as a buyer matters enormously. Factors like whether you have a property to sell, how quickly you can proceed, and whether you already have a mortgage agreement in principle all feed into the seller's thinking. A seller who is eager to move quickly may well prefer a slightly lower offer from a buyer who is ready to go. Understanding offer price nuances in the UK market gives you a clearer picture of how these dynamics play out.

Pro Tip: Always submit your offer in writing via email through the agent. This creates a clear paper trail and confirms the terms you are offering, including any conditions or inclusions.

Steps after offer acceptance

Once a seller accepts your offer, the clock starts ticking. The post-acceptance period typically spans 30 to 60 days and involves a sequence of parallel tasks, any one of which can cause delays if not handled promptly.

-

Instruct a solicitor or conveyancer. Do this within days of acceptance, not weeks. Your solicitor handles the legal transfer of ownership, conducts searches, and raises enquiries with the seller's solicitor.

-

Finalise your mortgage application. If you have a mortgage in principle, your lender now needs the property details to issue a formal offer. Gather payslips, bank statements, and any other documentation your lender requires.

-

Commission a property survey. There are several survey types available in the UK. A basic mortgage valuation protects the lender, not you. A homebuyer's report or a full structural survey gives you a far clearer picture of the property's condition and any potential costs. Reviewing your UK property purchase checklist at this stage keeps you organised.

-

Searches and enquiries. Your solicitor will order local authority searches, environmental searches, and drainage searches. These reveal anything from planning permissions nearby to flood risk and contaminated land.

-

Review the draft contract. Your solicitor will review the draft contract sent by the seller's solicitor, raise any questions, and negotiate the terms before you reach exchange.

-

Exchange contracts. This is the point at which both parties are legally committed. You pay a deposit, typically 10% of the purchase price, and a completion date is set.

-

Completion. The remaining funds are transferred, and ownership passes to you.

Pro Tip: Ask your solicitor for a realistic timeline at the outset. Chain length, local authority search turnaround times, and lender processing speeds all affect how long each stage takes. Having this context early prevents unnecessary anxiety.

How sellers assess and compare offers

Price is the headline, but it rarely tells the whole story. Sellers often prefer a dependable buyer with a mortgage in principle over one offering a higher price but with financing uncertainties. This is one of the most underappreciated truths in the UK property market.

The table below shows what sellers typically weigh when comparing offers side by side.

| Factor | Why it matters to sellers |

|---|---|

| Offer price | The starting point, but not the only consideration |

| Mortgage in principle | Signals that a lender has already assessed the buyer's affordability |

| Chain status | A chain-free buyer reduces the risk of the sale falling through |

| Completion flexibility | Matching the seller's preferred timeline can tip the balance |

| Proof of funds | Cash buyers or buyers with deposits readily available offer speed and certainty |

| Buyer attitude | Cooperative, communicative buyers reduce perceived transaction risk |

A seller who has already had one sale fall through due to a buyer's financing issues will almost certainly favour security over an extra few thousand pounds on the asking price. Asking whether a seller has pre-approval requests from their agent is a signal they are taking your offer seriously.

Non-price terms such as agreeing to purchase with existing fixtures included, committing to a specific completion timeline, or waiving certain survey conditions can be equally persuasive in competitive situations.

Negotiation nuances and handling counteroffers

Receiving a counteroffer is not a setback. It is a signal that the seller is engaged and wants to do business. How you respond determines whether the deal moves forward or stalls. A well-prepared property negotiation strategy makes this stage far less stressful.

One thing experienced buyers learn quickly is that silence after an offer is strategic, not dismissive. Sellers often wait 24 to 48 hours before responding, particularly when they want to signal confidence or give themselves space to weigh up competing interest. Do not interpret a delayed response as a rejection and rush to improve your offer unnecessarily.

Here are the key principles for handling counteroffers and negotiation periods effectively:

- Set an expiry on your offer. A response timeframe of 24 to 72 hours creates reasonable urgency. Leaving an offer open indefinitely allows the seller to use it as leverage while fielding other bids.

- Negotiate non-price terms first. Before raising your price, explore whether adjustments to the completion date, included items, or contingencies could resolve the impasse.

- Know your ceiling. Decide your maximum figure before you enter negotiations, not during them. Emotional decision-making under pressure leads to overpaying.

- Avoid premature withdrawal. Pulling an offer after a short silence can close a door that was about to open. Give the seller a reasonable window to respond.

- Use your agent. The estate agent represents the seller, but they want the deal done. They can often provide useful intelligence about what the seller actually needs from the transaction.

Pro Tip: When countering, move in deliberate increments rather than jumping straight to your maximum. Each increment signals willingness to negotiate while preserving room to manoeuvre.

Avoiding pitfalls and securing the sale

Offer acceptance creates momentum, but it does not guarantee completion. Gazumping, where a seller accepts a higher offer from another buyer after already accepting yours, remains a genuine risk in the UK. It is entirely legal until contracts are exchanged. Moving quickly is your best protection.

Here are the concrete steps to take immediately after acceptance:

- Instruct your solicitor the same day. Every day of delay is a day in which another buyer could enter the picture.

- Contact your mortgage broker or lender. Submit your full application without waiting to see if anything changes.

- Book your survey promptly. Surveyors can be booked up weeks in advance. Securing a slot early keeps your timeline on track.

- Request a lockout or exclusivity agreement. While not standard practice in England and Wales, some sellers will agree to a period of exclusivity in exchange for a goodwill deposit. This gives you legal protection if the seller accepts another offer during the agreed period.

- Maintain regular contact with the estate agent. Staying visible and cooperative throughout the process reassures the seller that you are committed, which reduces the temptation to consider alternative buyers.

Prompt conveyancing and consistent communication are the most effective tools a buyer has. Deals that stall tend to attract opportunists. Deals that move steadily forward tend to close.

My take on what buyers consistently get wrong

I have seen enough property transactions to know that most buyers enter the offer stage thinking purely about price. They agonise over whether to offer £5,000 above or below the asking price, and almost completely ignore the factors that sellers actually use to decide between competing buyers.

In my experience, the buyers who succeed in competitive markets are the ones who have done their preparation before they even view the property. They have their mortgage in principle ready. They have a solicitor on standby. They know exactly how much they can spend and they are not making that up as they go.

What I find equally striking is how badly buyers handle the waiting period. Silence from a seller is not a no. It is nearly always deliberate. A seller who has had your offer for 36 hours without responding is almost certainly still thinking, not ignoring you. The buyers who panic and either raise their offer immediately or withdraw entirely are the ones who hand away negotiating leverage for nothing.

My honest advice is to treat the period between offer and exchange as a project you are managing, not a situation that is happening to you. Instruct your solicitor immediately. Stay in contact with the agent. Book your survey early. The buyers who stay organised and visible are far less likely to be gazumped or to lose a deal to avoidable delays.

The other thing worth saying plainly: a lower offer that is clean, well-prepared, and backed by a mortgage in principle will frequently beat a higher offer from a buyer who still needs to arrange finance. Do not focus only on the number. Focus on preparing a winning offer that gives the seller every reason to say yes and stay committed.

— Rhys

Know your numbers before you offer

Understanding how property offer acceptance works is only part of the picture. The other part is making sure your offer is grounded in real market data, not guesswork or optimism.

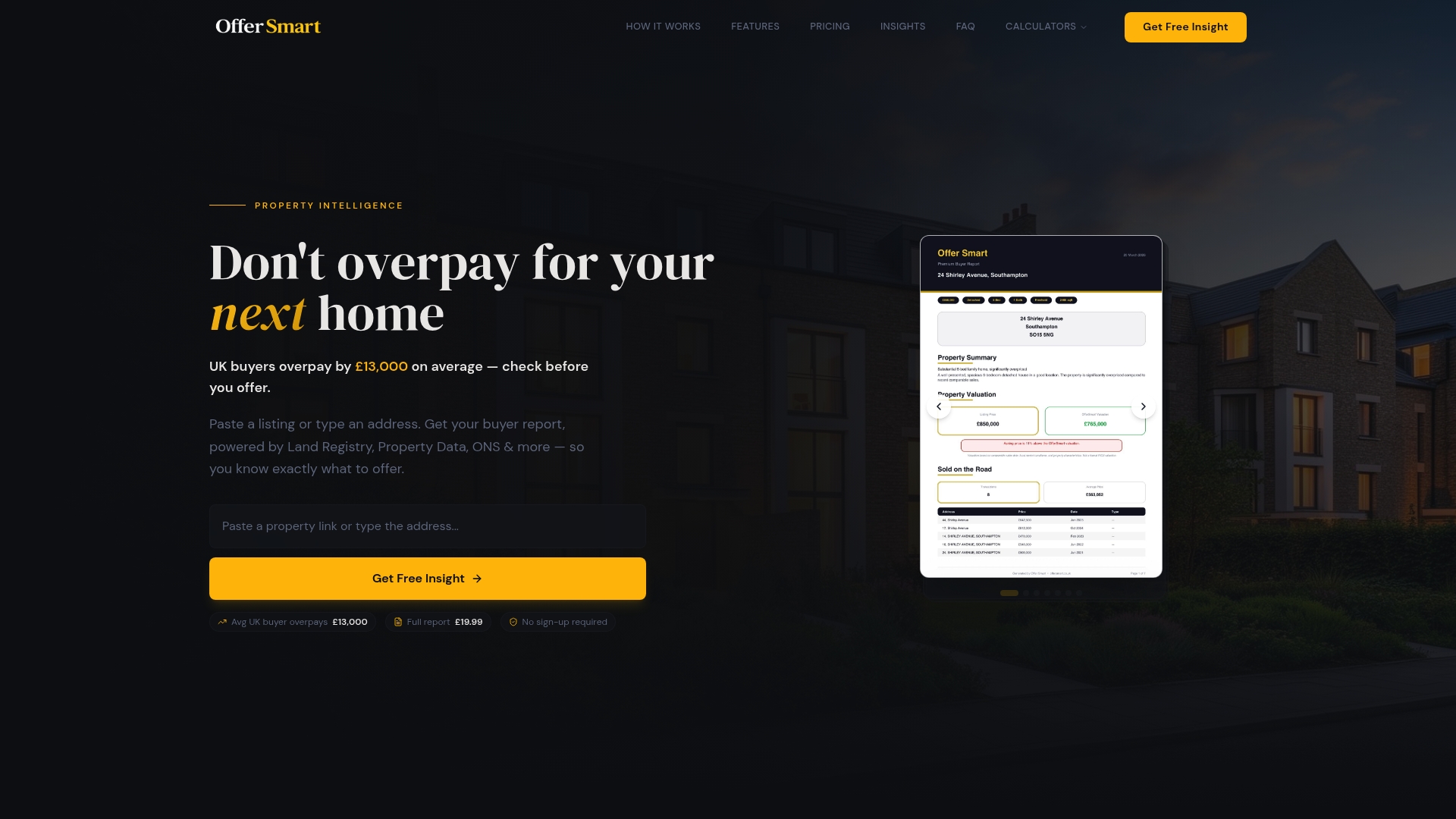

Offersmart is built specifically for UK buyers who want to go into negotiations with confidence. Enter a property address or paste a listing link, and Offersmart analyses comparable sales on the same road, calculates what you should realistically offer, and flags key risks including flood risk, crime rates, and local amenity scores. For investors, it also provides rental yield estimates and projected ROI. Use the mortgage calculator to understand your monthly costs before submitting anything. Then use the full suite of buyer tools to build an offer backed by data. No overpaying. No second-guessing.

FAQ

Is an accepted offer legally binding in the UK?

No. In England and Wales, an accepted offer is not legally binding until contracts are exchanged. Either party can withdraw before that point without legal penalty.

How long does the process take after offer acceptance?

Post-acceptance completion typically takes 30 to 60 days, though chain length, survey findings, and lender processing times can extend this considerably.

What is gazumping and can I prevent it?

Gazumping occurs when a seller accepts a higher offer from another buyer after already accepting yours. You can reduce the risk by moving quickly on legal and mortgage steps and by requesting an exclusivity agreement from the seller.

Can I negotiate after my offer is accepted?

Yes. If a survey reveals significant issues, you may have grounds to renegotiate the price before exchanging contracts.

What makes a seller choose a lower offer over a higher one?

A lower but secure offer from a chain-free buyer with a mortgage in principle often wins over a higher bid with financing uncertainty, especially if the seller has already experienced a failed sale.