Making a competitive offer on a house is defined as submitting a bid that combines a well-researched price with contract terms specifically tailored to what the seller values most. For first-time buyers in the UK, this distinction matters enormously. In 2026, with housing stock still tight across many regions and mortgage rates stabilising, buyers who rely on price alone routinely lose out to those with cleaner, better-structured offers. This guide covers how to determine the right price using comparable sales, which contract terms give you the strongest edge, and the mistakes that cost first-time buyers their dream home.

How to make a competitive offer: pricing with data, not emotion

The difference between the list price, the market value, and a competitive bid is not always obvious, but understanding all three is the foundation of any winning offer. The list price is what the seller wants. The market value is what comparable properties have actually sold for. Your competitive bid sits at the intersection of both, adjusted for current local conditions.

Start by gathering sold prices for similar properties within a half-mile radius over the last three to six months. Rightmove and the Land Registry both publish sold prices, and your conveyancer or estate agent can pull more granular data. Focus on properties with the same number of bedrooms, similar condition, and comparable plot size. A four-bedroom Victorian terrace in Leeds is not a useful comparable for a two-bedroom new-build flat in the same postcode.

Understanding local market conditions is equally critical. In a seller's market, where demand outstrips supply, competitive bids often land 3% to 8% above the asking price. In a balanced or buyer's market, you have more room to negotiate below asking. Knowing which environment you are operating in prevents both underbidding and unnecessary overbidding.

- Check sold prices on Rightmove and the Land Registry for the last three to six months

- Focus on properties with matching bedrooms, condition, and location

- Identify whether your target area is a seller's, balanced, or buyer's market

- Set a firm maximum price before viewing, not after falling in love with the property

- Use Offersmart to compare recent sales on the same road and get a data-backed offer range

Pro Tip: Set your walk-away number before you make any offer. Experts recommend basing offers on comparable sales, not on how much you want the property. Write the number down. Commit to it.

What makes a strong offer beyond the price?

Buyers who combine strong financial proof with flexible terms and a well-structured offer consistently outperform those relying on price alone. This is the single most important insight for first-time buyers to absorb before submitting anything.

Here are the key components to consider structuring into your offer:

-

Earnest money deposit. The standard deposit in the UK is typically 10% on exchange, but signalling seriousness earlier matters. In competitive situations, a deposit of 5% or higher demonstrates genuine financial commitment and can separate your offer from others at a similar price point.

-

Mortgage pre-approval. A decision in principle (DIP) from your lender is the UK equivalent of a US pre-approval letter. Verified mortgage pre-approval confirms your income, assets, and credit have been assessed, giving sellers confidence that your offer will not collapse at the mortgage stage.

-

Contingencies. In the UK, the formal exchange of contracts creates the legally binding agreement, but buyers routinely include conditions around survey results and mortgage approval in their offer letters. Limiting or removing these conditions makes your offer cleaner, though it increases your risk. Never waive protections without understanding the full financial exposure.

-

Flexible closing dates. Flexible closing timelines aligned with seller needs can outweigh small price differences. If the seller needs three months to find their next property, offering that timeline costs you nothing but could win you the house.

-

Escalation clauses. An escalation clause automatically increases your offer by a set increment above any competing bid, up to a maximum cap. Escalation clauses can be effective in multi-offer situations, though some sellers and agents view them with scepticism, preferring a clean best-and-final offer instead.

| Offer component | Competitive approach | Risk level |

|---|---|---|

| Earnest money deposit | 5% or higher to signal intent | Low to medium |

| Mortgage pre-approval | Full DIP from lender submitted with offer | Low |

| Survey contingency | Pre-offer survey to allow clean submission | Medium |

| Closing date | Match seller's preferred timeline | Low |

| Escalation clause | Set increment above rivals, capped at maximum | Medium |

Pro Tip: Ask your estate agent to find out the seller's preferred completion date before you submit. Matching it precisely costs nothing and signals that you have done your homework.

How to structure your offer to stand out in a bidding war

Winning house bidding strategies are rarely about the largest number. Sellers value offer packages — price plus terms — more than the highest bid alone. A clean offer with fewer complications frequently beats a higher but conditional one.

The following tactics give first-time buyers a genuine edge in multiple-offer situations:

- Use odd-dollar figures. Odd-number offers such as £427,500 suggest a carefully calculated bid rather than a round guess. Sellers and agents notice the difference, and it can subtly signal that you have done your research.

- Commission a pre-offer inspection. A pre-offer survey costs between £350 and £500 but allows you to submit a clean offer without a survey contingency while still knowing what you are buying. This is one of the most underused tactics among first-time buyers.

- Communicate seller priorities through your agent. Before submitting, ask your agent to speak with the seller's agent about what matters most: speed, certainty, price, or flexibility. Structuring your offer around those priorities is more effective than guessing.

- Write a short personal letter. A brief, factual note explaining why you want the property can create emotional connection without oversharing personal financial details. Keep it to three or four sentences and focus on the home itself.

| Tactic | Advantage | Potential drawback |

|---|---|---|

| Pre-offer survey | Removes survey contingency cleanly | Upfront cost of £350 to £500 |

| Odd-number offer price | Signals careful calculation | Minimal, mostly psychological |

| Personal buyer letter | Creates emotional appeal | Rarely decisive on its own |

| Matching seller's timeline | Reduces seller uncertainty | May require flexibility on your end |

For a detailed walkthrough of the full offer preparation process, Offersmart's blog covers each step with UK-specific guidance.

Common mistakes that cost first-time buyers the deal

The most expensive mistake in competitive property buying is emotional overbidding. Experienced agents stress the psychological discipline of setting a firm maximum offer before entering any negotiation, because the heat of a bidding war reliably pushes buyers past their sensible limit.

Beyond overbidding, there are several specific risks worth understanding clearly:

- Waiving the survey contingency without prior inspection. Removing this protection without first commissioning a survey exposes you to hidden structural costs. A pre-offer survey is the only safe way to submit a clean offer on this point.

- Ignoring the appraisal gap risk. If your lender's valuation comes in below your agreed offer price, you must cover the shortfall in cash or renegotiate. Buyers waiving appraisal contingencies must have liquid funds available, or they risk losing their deposit entirely.

- Making a non-refundable deposit. While attractive to sellers, a non-refundable earnest money deposit exposes you to significant financial loss if the deal falls through for reasons outside your control. This is generally not advisable for first-time buyers.

- Underestimating total costs. Stamp Duty Land Tax, solicitor fees, survey costs, and removal expenses add up quickly. Factoring these into your maximum offer figure prevents nasty surprises after exchange.

"The buyers who regret their purchase almost always made their final decision in an emotional state. The buyers who feel confident years later made their decision with a number written down before they ever walked through the door."

A property negotiation strategy built on data and clear financial limits is the most reliable protection against buyer's remorse.

Key takeaways

A competitive offer on a house requires a data-backed price, verified financial readiness, and contract terms structured around what the seller actually needs.

| Point | Details |

|---|---|

| Price from data, not emotion | Use comparable sold prices from the last three to six months to set your offer range. |

| Financial proof matters | A decision in principle submitted with your offer significantly increases seller confidence. |

| Terms can outweigh price | Flexible closing dates and a clean offer structure frequently beat higher but complicated bids. |

| Pre-offer survey removes risk | Commissioning a survey before offering lets you waive the contingency safely. |

| Set a walk-away number | Decide your maximum before viewing and commit to it regardless of competition. |

Why preparation beats price every time

I have spoken with enough first-time buyers to know that the ones who lose out rarely lose because their budget was too low. They lose because they submitted an offer that felt uncertain to the seller. A round-number bid with three conditions attached and no DIP in sight tells a seller one thing: this deal might fall apart.

The buyers who win in competitive markets are not always the ones offering the most money. They are the ones who have done the work before submitting. They know the comparable sales. They have their mortgage agreed in principle. They have thought about what the seller needs and built that into their offer. That preparation is visible in the offer document, and sellers and their agents feel it immediately.

My honest view is that first-time buyers underestimate how much control they actually have in this process. You cannot always control the competition, but you can control the quality and credibility of your offer. Focus there. Get the financial paperwork sorted first. Research the street, not just the property. And set your maximum price before you fall in love with the place.

There will always be more properties. There will not always be another chance to protect your finances by staying disciplined.

— Rhys

Get a data-backed offer figure before you bid

Knowing what to offer is the hardest part of the process for most first-time buyers. Offersmart removes the guesswork by analysing recent comparable sales on the same road, assessing flood risk, crime data, and local amenities, and giving you a clear picture of what the property is genuinely worth.

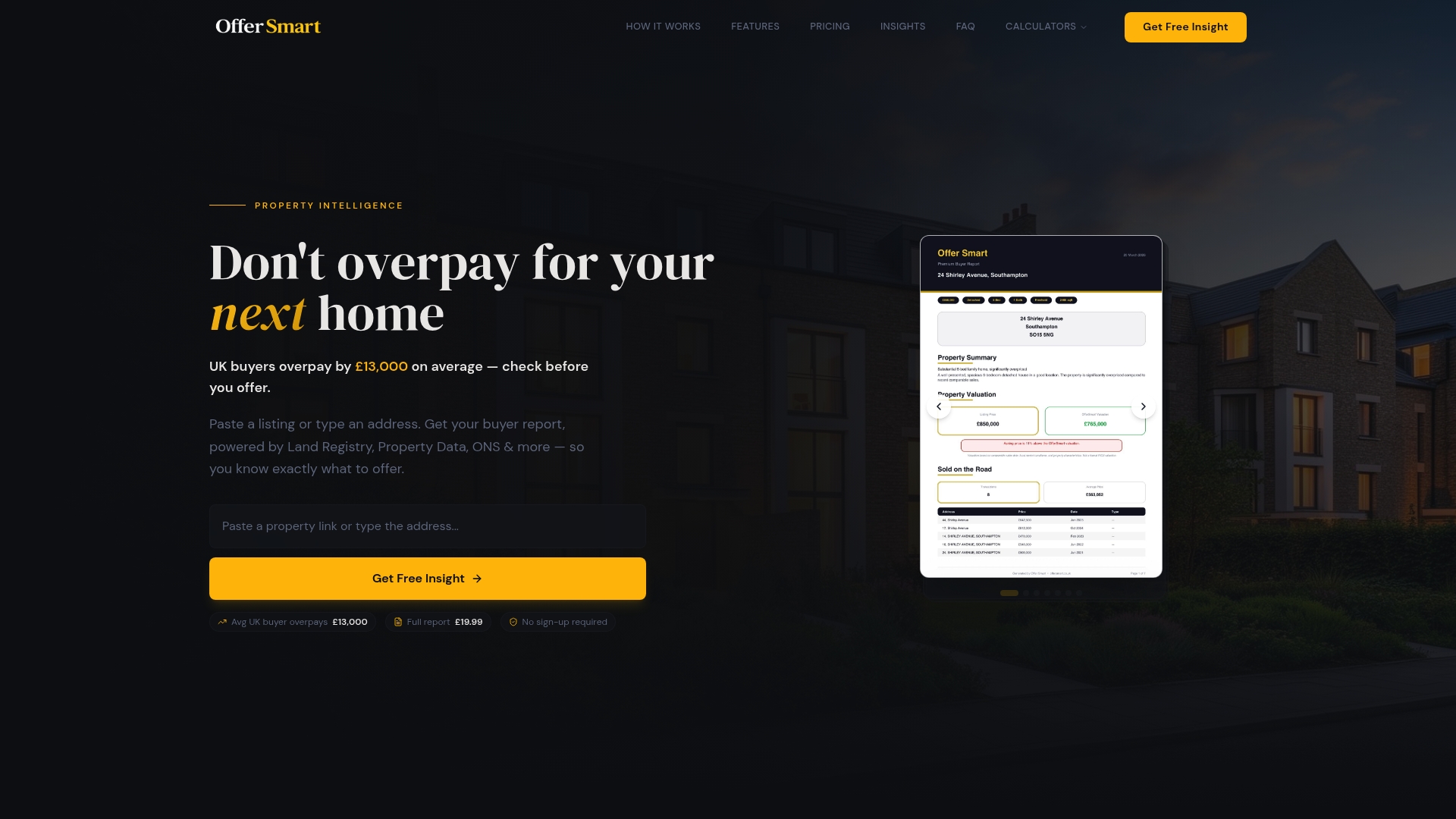

Before you submit your next offer, use the Offersmart mortgage calculator to confirm your borrowing capacity and monthly costs. Enter a property address or paste a listing link, and Offersmart instantly generates a buyer report with a realistic offer range, a five-year value forecast, and full local data. You will know exactly what to offer and why, before anyone else does.

FAQ

What is a competitive offer on a house in the UK?

A competitive offer is a bid that combines a well-researched price with contract terms tailored to the seller's priorities, such as flexible completion dates and verified mortgage approval. Price alone rarely wins in a competitive market.

How much above asking price should I offer?

In a seller's market, competitive bids typically land 3% to 8% above asking price, based on comparable sold prices in the area. In a balanced or buyer's market, offers at or slightly below asking are often accepted.

Should I waive the survey contingency to win a bidding war?

Only waive the survey contingency if you have already commissioned a pre-offer inspection, which costs between £350 and £500. Waiving it without prior knowledge of the property's condition exposes you to serious financial risk.

What is an escalation clause and should I use one?

An escalation clause automatically increases your offer by a set increment above any competing bid, up to a maximum cap. It can be effective in multi-offer situations, but some sellers prefer a straightforward best-and-final figure instead.

How does a decision in principle help my offer?

A decision in principle (DIP) from your lender confirms that your income, credit, and assets have been assessed, giving sellers confidence that your offer is financially credible and unlikely to fall through at the mortgage stage.