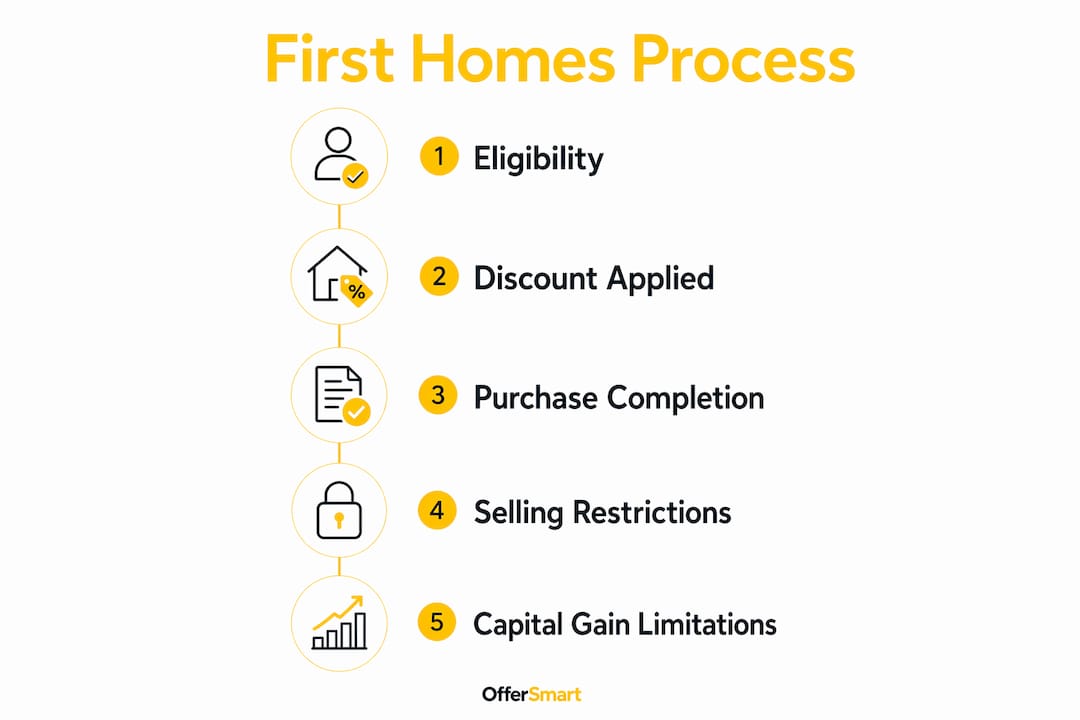

The First Homes Scheme is a government-backed programme that gives eligible first-time buyers in England a permanent discount of at least 30% off the market value of a new-build home. That discount does not disappear when you sell. It stays with the property, passing to the next eligible buyer at the same percentage reduction. For anyone struggling to bridge the gap between their savings and rising property prices, this scheme is one of the most direct forms of first-time buyer assistance available in England today.

The scheme sits alongside Help to Buy and Shared Ownership as part of the government's affordable housing toolkit, but it works differently from both. Rather than offering a loan or a part-ownership arrangement, it simply reduces the purchase price permanently. That distinction matters enormously when you are planning your finances and thinking about what you can realistically afford.

What is the First Homes Scheme and who qualifies?

The First Homes Scheme is defined by the Ministry of Housing, Communities and Local Government as an England-only affordable housing programme targeting first-time buyers on modest incomes. To qualify, you must meet several criteria simultaneously, and missing any one of them disqualifies your application.

The eligibility rules are as follows:

- First-time buyer status: You must never have owned a residential property in the UK or abroad, in line with HMRC's definition of a first-time buyer.

- Household income cap: Your combined household income must not exceed £80,000 per year, or £90,000 if you are buying in London. The income eligibility rules apply to all adults who will be named on the mortgage.

- Mortgage requirement: You must fund at least 50% of the discounted purchase price with a mortgage or regulated home purchase plan. Cash-only buyers are excluded.

- Local connection rules: Many local authorities add a further layer of criteria based on where you live, work, or have family ties. These are defined through Section 106 agreements and vary significantly by area.

- Key worker priority: Local authorities may prioritise key workers such as NHS staff, teachers, and emergency service workers during an initial three-month sales period before the property opens to all eligible buyers.

Pro Tip: Check your local authority's specific connection criteria before you fall in love with a particular development. Local connection rules act as a gate in the application process and can override national eligibility even if you meet every other requirement.

Typical mortgage deposits for First Homes purchases can be as low as 5% of the discounted price, which meaningfully reduces the upfront cash you need to save. That said, you still need a lender willing to offer a mortgage on a property with a legal covenant attached, so specialist mortgage advice is worth seeking early.

How does the discount work, and what happens when you sell?

The First Homes Scheme offers a discount of 30% to 50% off the open market value of a new-build home. The minimum is 30%, but local authorities can increase this to 50% if local affordability pressures justify it. That flexibility means the same scheme can deliver very different savings depending on where you buy.

The discount is not a loan. It is enforced through a legal covenant registered on the property title, which means it runs with the land in perpetuity. When you come to sell, the process works in three steps:

- Independent valuation: A RICS-registered surveyor assesses the open market value of your home at the point of sale. This independent valuation process prevents sellers from inflating the price to reduce the effective discount.

- Discount calculation: The same percentage discount applied when you bought is applied to the new valuation. If you bought with a 30% discount and the market value has risen to £300,000, your maximum sale price is £210,000.

- Eligible buyer only: You can only sell to another buyer who meets the First Homes eligibility criteria at the time of sale.

Here is how the First Homes Scheme compares to the two other main government-backed routes:

| Feature | First Homes Scheme | Help to Buy (closed 2023) | Shared Ownership |

|---|---|---|---|

| Mechanism | Permanent price discount | Government equity loan | Part-buy, part-rent |

| Discount or loan | Discount | Loan (repayable) | Neither |

| Resale restriction | Yes, discount passes on | No | Yes, to housing association |

| Capital gains | Proportional only | Full on owned share | Full on owned share |

| New-build only | Yes | Yes | Yes |

The capital gains point deserves attention. Because the discount limits equity gain proportionally, you will not benefit from the full rise in market value when you sell. If the market rises by £50,000, you capture only 70% of that gain on a 30% discount property. That trade-off is the price of the initial affordability benefit.

Pro Tip: The conveyancing process for a First Homes property is more complex than a standard sale due to the legal covenant. Use a solicitor with direct experience of First Homes transactions to avoid delays.

Where can you find First Homes properties?

Availability is the scheme's most practical constraint. First Homes properties are only available on selected new-build developments where developers have agreed with the local authority to designate a proportion of plots as First Homes. Not every new development includes them, and supply in any given area can be limited.

Price caps apply after the discount is applied:

- £250,000 maximum in England (outside London)

- £420,000 maximum in Greater London

These caps mean the scheme is most accessible in areas where new-build prices are moderate. In high-demand cities outside London, the cap can still exclude many developments once you work backwards from the discounted price to the original market value.

To find available properties, you can:

- Search Rightmove and Zoopla using the "First Homes" filter under new-build listings

- Contact your local authority's housing team directly, as some areas maintain waiting lists or notify registered buyers when new plots are released

- Visit developer websites for housebuilders such as Barratt Homes, Persimmon, and Taylor Wimpey, all of whom have participated in the scheme

- Register with Help to Buy agents in your region, who hold information on upcoming First Homes releases

The application process itself runs through the developer and local authority rather than a central government portal. You will typically need to provide proof of income, evidence of first-time buyer status, and documentation supporting any local connection claim. During the initial three-month priority period, local authorities may require additional evidence if key worker or local connection criteria apply.

Pro Tip: Set up property alerts on Rightmove and Zoopla specifically for new-build homes in your target area. First Homes plots are released in small batches and sell quickly, so early notification gives you a real advantage.

For a broader picture of what to expect at each stage of your purchase, the homebuying process timeline guide from Offersmart walks you through each step clearly.

What are the benefits and limitations of the First Homes Scheme?

The scheme delivers genuine advantages for buyers who fit the criteria, but it also carries trade-offs that are worth understanding before you commit.

Key benefits:

- A minimum 30% reduction in purchase price directly lowers the deposit you need to save

- The permanent nature of the discount means the home remains affordable for future buyers, not just you

- Mortgage deposits as low as 5% of the discounted price reduce the barrier to entry significantly

- Unlike Help to Buy, there is no loan to repay and no interest charges building up over time

- The scheme is unlike Shared Ownership in that you own 100% of the property from day one, with no rent payable on a remaining share

Practical limitations:

- Restricted equity gain on resale means the scheme suits buyers prioritising stability over maximum investment return

- Local connection rules can exclude buyers who meet all national criteria but lack ties to the specific area

- Supply is limited to designated plots, so you cannot simply choose any new-build home

- The legal covenant adds complexity to future sales and requires specialist conveyancing

"The First Homes Scheme works best for buyers who plan to stay in the property for a meaningful period and value affordability now over maximum capital return later. It is not the right route for everyone, but for the right buyer in the right location, it removes a significant financial barrier."

For buyers weighing up whether to proceed with a survey before making an offer, the property surveys guide for first-time buyers covers what to expect on new-build homes specifically.

How does the First Homes Scheme differ across the UK?

The First Homes Scheme is England-only. Scotland, Wales, and Northern Ireland each operate separate programmes with different mechanisms, and the naming similarities cause genuine confusion among buyers.

| Nation | Scheme name | Mechanism | Key difference |

|---|---|---|---|

| England | First Homes Scheme | Permanent price discount | Discount runs with the property title |

| Scotland | First Home Fund | Shared equity loan | Government takes an equity stake, not a discount |

| Wales | Help to Buy Wales | Shared equity loan | Welsh Government loan up to 20% of purchase price |

| Northern Ireland | Co-Ownership | Part-buy, part-rent | Similar to Shared Ownership in England |

Scotland's First Home Fund provides shared equity loans rather than permanent discounts, meaning the Scottish Government retains a financial interest in the property. That is a fundamentally different arrangement from the England scheme, despite the similar name. Many first-time buyers confuse these schemes, which can lead to misapplication and wasted time. If you are buying in Scotland, Wales, or Northern Ireland, the England-based First Homes Scheme does not apply to you.

Key takeaways

The First Homes Scheme gives eligible first-time buyers in England a permanent, legally enforced discount of 30% to 50% on new-build homes, reducing both the purchase price and the deposit required.

| Point | Details |

|---|---|

| Permanent discount | The 30% to 50% reduction stays with the property and passes to the next eligible buyer on resale. |

| Income eligibility | Household income must be below £80,000 (£90,000 in London) to qualify nationally. |

| Local connection rules | Section 106 criteria set by local authorities can restrict access even when national rules are met. |

| Price caps apply | After discount, homes must cost no more than £250,000 in England or £420,000 in London. |

| England only | The scheme does not apply in Scotland, Wales, or Northern Ireland, which have separate programmes. |

The trade-off most buyers overlook

From what I have seen working with first-time buyers navigating government schemes, the First Homes Scheme is genuinely underused. Most buyers default to Shared Ownership without fully understanding that First Homes gives you 100% ownership from day one, with no rent on a remaining share and no equity loan to repay.

The trade-off that catches people off guard is the restricted capital gain. Buyers who purchase expecting to build the same equity as a standard homeowner are sometimes disappointed when they come to sell. The covenant is not a hidden catch. It is the mechanism that makes the discount possible. Understanding it upfront changes how you plan your next move.

My strongest advice is to treat local connection rules as your first filter, not your last. I have seen buyers spend weeks researching a specific development only to discover they do not qualify under the local authority's Section 106 criteria. Check that first. Then check the price caps. Then look at mortgage availability on covenant-restricted properties, because not every lender is comfortable with them.

The conveyancing complexity is real but manageable. Use a solicitor who has completed First Homes transactions before. The legal covenant requires specific handling, and a solicitor unfamiliar with it will slow the process down considerably.

— Rhys

How Offersmart helps you buy with confidence

Once you know you qualify for the First Homes Scheme, the next question is whether the specific property you are considering is priced fairly, even after the discount. Offersmart analyses comparable local sales, flood risk, crime data, and area lifestyle factors to give you a clear picture of true market value before you make an offer. Use the mortgage calculator to model your affordability against the discounted purchase price, and explore the full property calculators to understand running costs and long-term value. For practical guidance on structuring your offer once you have found the right home, the winning offer guide from Offersmart gives you a clear, step-by-step approach.

FAQ

What is the First Homes Scheme in simple terms?

The First Homes Scheme is an England-only government programme that lets eligible first-time buyers purchase a new-build home at a minimum 30% discount off market value. The discount is permanent and passes to the next buyer when the home is sold.

Who is eligible for the First Homes Scheme?

You must be a first-time buyer with a household income below £80,000 (£90,000 in London), use a mortgage covering at least 50% of the discounted price, and meet any local connection criteria set by the relevant local authority.

Does the First Homes Scheme apply in Scotland or Wales?

No. The First Homes Scheme is England-only. Scotland operates the First Home Fund as a shared equity loan, and Wales runs Help to Buy Wales, both of which work differently from the England discount model.

Can I make a full capital gain when I sell a First Homes property?

No. Because the discount is permanent, you only benefit proportionally from market price increases. If the market rises by £50,000 and your discount is 30%, your maximum gain is 70% of that increase.

How do I apply for the First Homes Scheme?

Applications are made through the developer and local authority for a specific designated development, not through a central government portal. You will need proof of income, first-time buyer status, and any local connection documentation required by the local authority.